The Real Reason Chinese EVs Are So Cheap (It's Not Subsidies)

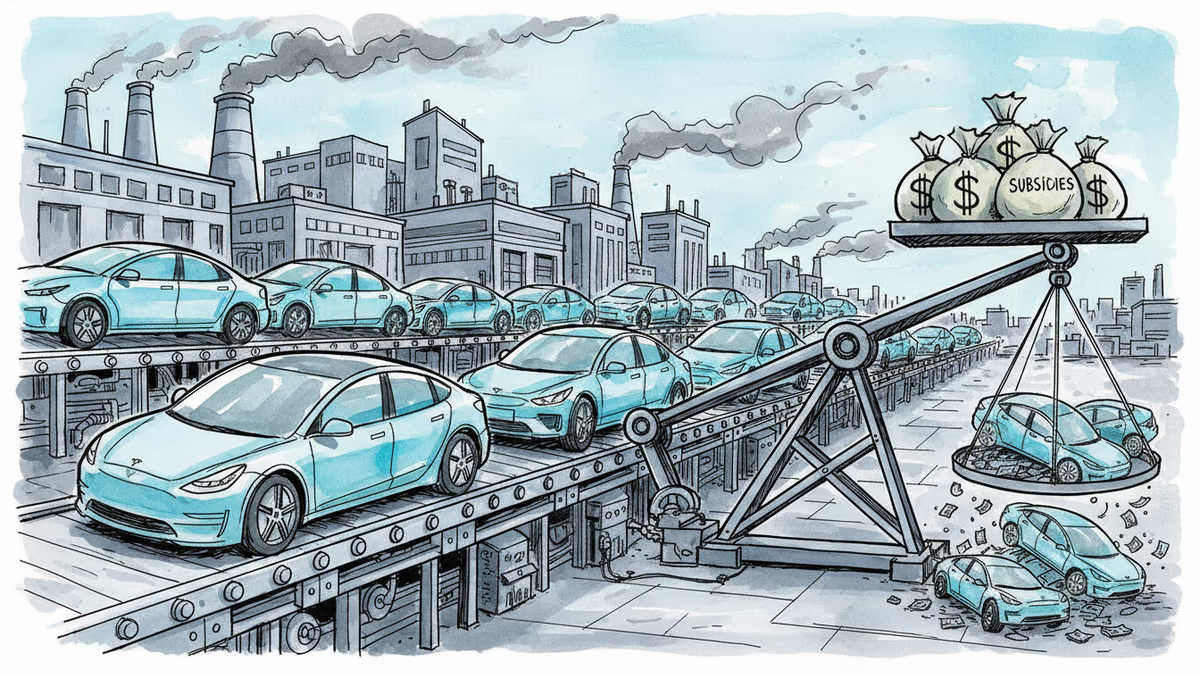

Western automakers lost two-thirds of China's EV market share. Everyone blames subsidies, but they account for just 5% of BYD's $4,700 cost advantage over Tesla. The real story is structural.

Everyone Got It Wrong About Chinese EVs

Western carmakers just got schooled in China, and it wasn't by government handouts.

Their share of China's EV market collapsed from two-thirds in 2020 to barely one-third last year. The knee-jerk explanation? Chinese state subsidies are flooding the market with artificially cheap cars. But a bombshell February 19 report from New York's Rhodium Group reveals that's mostly fiction.

Consider the tale of two sedans: BYD's Seal and Tesla's Model 3. Between 2022 and 2025, BYD slashed the Seal's price from $30,198 to $24,190 — a $6,008 drop. Tesla's Shanghai-made Model 3? It barely budged, falling a measly $221 from $32,909.

Here's the kicker: Of BYD's $4,700 per-vehicle cost advantage over Tesla, Chinese state subsidies account for just 5%. The other 95% comes from something far more fundamental — and harder to counter.

The Subsidy Myth Crumbles

Don't get it wrong — Beijing does favor its own. BYD's subsidies jumped from 26% of net income in 2024 to 35% in 2025. Meanwhile, Tesla has reported zero subsidy income since 2021. But as Rhodium puts it: "Subsidies matter, but less than often assumed."

The real gap lies in structural advantages that would make any MBA student weep with envy.

Chinese manufacturers spend substantially less per vehicle on R&D and administrative costs. BYD actually has higher absolute R&D spending, but spreads it across far more vehicles. Plus, Chinese engineering talent costs a fraction of what Western companies pay — and there's more of it.

The Payment Game Changer

Here's where it gets interesting for Western executives: Chinese OEMs have mastered the art of delayed supplier payments. While Western companies typically pay suppliers within 30-60 days, Chinese firms stretch this to months.

Rhodium estimates this practice alone gives BYD a $214 per vehicle cost advantage and Geely$83 per vehicle — assuming they'd otherwise need to borrow to match Western payment cycles.

Try explaining that strategy to your suppliers in Detroit or Stuttgart.

The Vertical Integration Advantage

Chinese manufacturers didn't just build cars; they built ecosystems. In-house manufacturing of major components, preferential financing terms, and unpaid licensing agreements all add layers of cost savings that Western competitors can't easily replicate.

Most foreign brands already manufacture locally in China, yet still can't compete on price. The gap stems from deeper vertical integration and greater scale that took decades to build.

The Western Dilemma

Here's the brutal truth Western automakers face: Closing the cost gap would require a strategy that puts them at odds with their own governments.

"Closing the cost gap would require Western OEMs to follow a difficult path," the report states. "Investing more deeply in China to build local R&D and supplier ties, while cutting costs and jobs at home."

That strategy increasingly conflicts with Western industrial policies designed to protect domestic auto employment and value creation. Ford and GM can't exactly tell Washington they're moving more operations to China to compete with BYD.

The Regulatory Trap

Western firms face structural barriers their Chinese competitors don't. Home governments encourage domestic manufacturing under regulatory frameworks that prioritize local jobs over global competitiveness.

It's a classic catch-22: To compete with Chinese EVs, Western automakers need to adopt Chinese-style efficiency. But doing so would clash with their governments' "bring manufacturing home" policies.

The answer might determine which economic model wins the 21st century.

Authors

Related Articles

Waymo's new Ojai robotaxi isn't just a vehicle upgrade. It's the company's most serious attempt yet at cracking the cost problem that has kept autonomous vehicles from scaling. Here's what's really at stake.

China is restricting AI researchers and startup founders from traveling abroad as the U.S.-China AI performance gap narrows to just 2.7%. What Beijing's talent lockdown means for the global AI race.

The Ferrari Luce is finally here — 1,000 hp, a 122 kWh battery, and an interior designed by the team behind the iPhone. But the real story is what Ferrari risked to build it.

Mercedes-AMG's new GT 4-door coupe packs three YASA axial flux motors producing 1,153 hp and 1,475 lb-ft of torque. Here's what it means for the EV performance race—and who actually wins.

Waymo's new Ojai robotaxi isn't just a vehicle upgrade. It's the company's most serious attempt yet at cracking the cost problem that has kept autonomous vehicles from scaling. Here's what's really at stake.

China is restricting AI researchers and startup founders from traveling abroad as the U.S.-China AI performance gap narrows to just 2.7%. What Beijing's talent lockdown means for the global AI race.

The Ferrari Luce is finally here — 1,000 hp, a 122 kWh battery, and an interior designed by the team behind the iPhone. But the real story is what Ferrari risked to build it.

Mercedes-AMG's new GT 4-door coupe packs three YASA axial flux motors producing 1,153 hp and 1,475 lb-ft of torque. Here's what it means for the EV performance race—and who actually wins.

Thoughts

Share your thoughts on this article

Sign in to join the conversation