Kalshi Bet on Growth. Its Users Bet on Death. Now There's a Lawsuit.

A class action lawsuit accuses Kalshi of changing payout rules after Iran's Supreme Leader Khamenei was killed. The case cuts to the heart of prediction market credibility.

The bet was straightforward: when would Iran's Supreme Leader Ali Khamenei leave office? Last month, he was killed in strikes on Iran. The answer, it seemed, had arrived. The payout, however, did not.

A class action lawsuit filed last week alleges that Kalshi, one of the most prominent regulated prediction market platforms in the United States, failed to pay out on wagers related to Khamenei's departure from power. The core claim: Kalshi did not include a "death carveout" in its contract terms before Khamenei died, and only added that provision afterward. Users who believed death clearly qualified as "leaving office" say the platform retroactively changed the rules of a game already in play.

What Prediction Markets Promise — And What This Case Tests

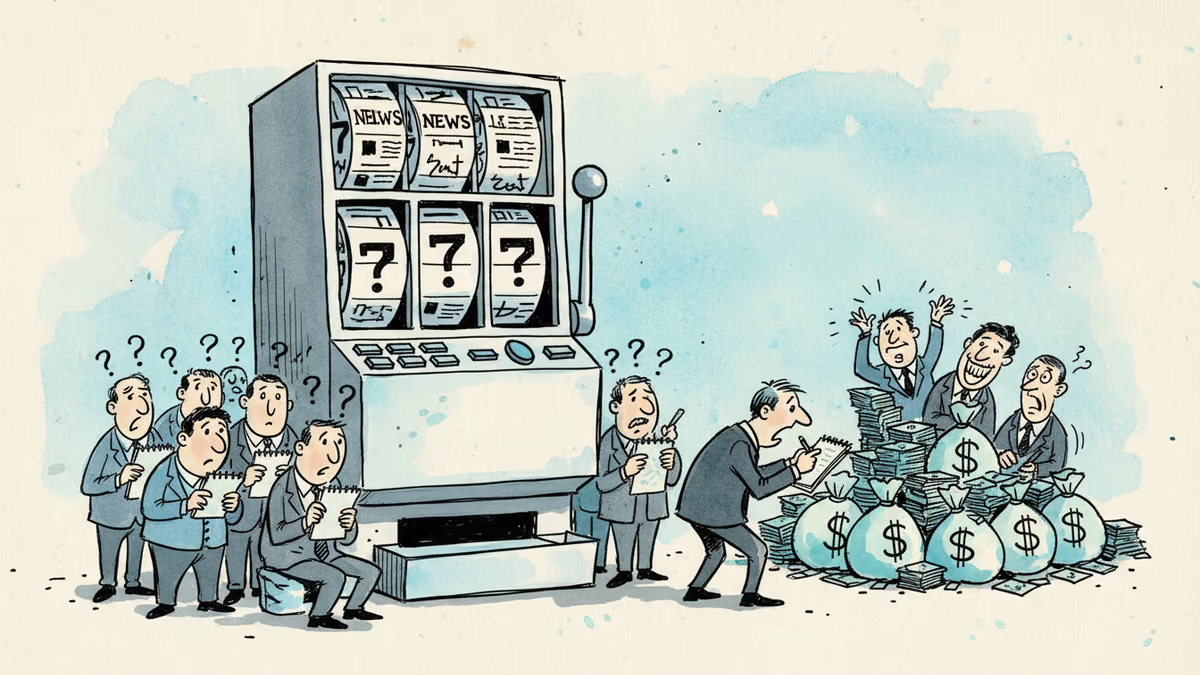

Kalshi isn't a back-alley sportsbook. It operates under the oversight of the Commodity Futures Trading Commission (CFTC) and has positioned itself as a legitimate financial tool — a platform where collective intelligence prices in real-world outcomes. It surged in visibility during the 2024 U.S. presidential election, when its markets were cited alongside traditional polling data.

That legitimacy rests entirely on one thing: trust in the settlement process. If users can't rely on a platform to pay out when conditions are met — or at least to define those conditions unambiguously in advance — the entire premise collapses. The Khamenei case exposes a structural vulnerability that goes beyond one disputed payout. Who decides what "counts"? And when is that decision made?

The ambiguity here wasn't trivial. Whether death constitutes removal from office is a genuinely interpretable question. But the cost of that ambiguity was borne entirely by users, not the platform. That asymmetry is what the lawsuit is really about.

Growing the Pie While the Pie Is on Fire

The timing is striking. At the same moment Kalshi is facing legal pressure from existing users, it's actively courting new ones. The Wall Street Journal reported Sunday that the share of women on Kalshi's platform has doubled over the past 10 months, part of a deliberate push to broaden its user base beyond its traditionally male-skewing demographic.

This isn't incidental. Prediction markets, like many financial products, suffer from a participation problem: the more diverse and numerous the participants, the more accurate and liquid the market becomes. Losing credibility with existing users doesn't just hurt retention — it degrades the product itself.

The growth story and the lawsuit are, in this sense, in direct tension. Kalshi is trying to become a mainstream financial platform. Mainstream financial platforms don't survive if users believe the house can rewrite the rules mid-game.

How Different Stakeholders Read This

For regulators, this is a test case. The CFTC has been cautiously permissive with prediction markets, allowing Kalshi to operate where others couldn't. A high-profile payout dispute involving a geopolitical event — and one as sensitive as the death of a foreign head of state — invites scrutiny of whether existing oversight frameworks are adequate.

For investors in Kalshi and the broader prediction market space, the lawsuit is a stress test of the business model. The company's valuation depends on continued growth and regulatory goodwill. Both are now under pressure simultaneously.

For users, especially newer ones being recruited through the platform's outreach efforts, the question is simpler: can I trust that if I'm right, I'll get paid?

For critics of prediction markets, this is familiar territory. They've long argued that these platforms introduce the language of financial instruments without the consumer protections that come with regulated financial products. This case may strengthen that argument in legislative circles.

Authors

Related Articles

A US special forces soldier involved in the operation that captured Venezuela's Maduro allegedly used classified intel to bet on Polymarket, pocketing over $400,000. The case exposes a gaping hole in how prediction markets are regulated.

Despite fierce competition, the CEOs of Polymarket and Kalshi have co-invested in 5(c) Capital, a $35M VC fund targeting prediction market infrastructure. What this signals for the industry.

Indonesia introduces age-tiered social media restrictions, allowing 13+ for low-risk platforms and 16+ for high-risk ones. How does this compare to Australia's blanket ban?

As Polymarket and Kalshi expand news partnerships, insider trading concerns mount. The line between gambling and information is blurring dangerously.

A US special forces soldier involved in the operation that captured Venezuela's Maduro allegedly used classified intel to bet on Polymarket, pocketing over $400,000. The case exposes a gaping hole in how prediction markets are regulated.

Despite fierce competition, the CEOs of Polymarket and Kalshi have co-invested in 5(c) Capital, a $35M VC fund targeting prediction market infrastructure. What this signals for the industry.

Indonesia introduces age-tiered social media restrictions, allowing 13+ for low-risk platforms and 16+ for high-risk ones. How does this compare to Australia's blanket ban?

As Polymarket and Kalshi expand news partnerships, insider trading concerns mount. The line between gambling and information is blurring dangerously.

Thoughts

Share your thoughts on this article

Sign in to join the conversation