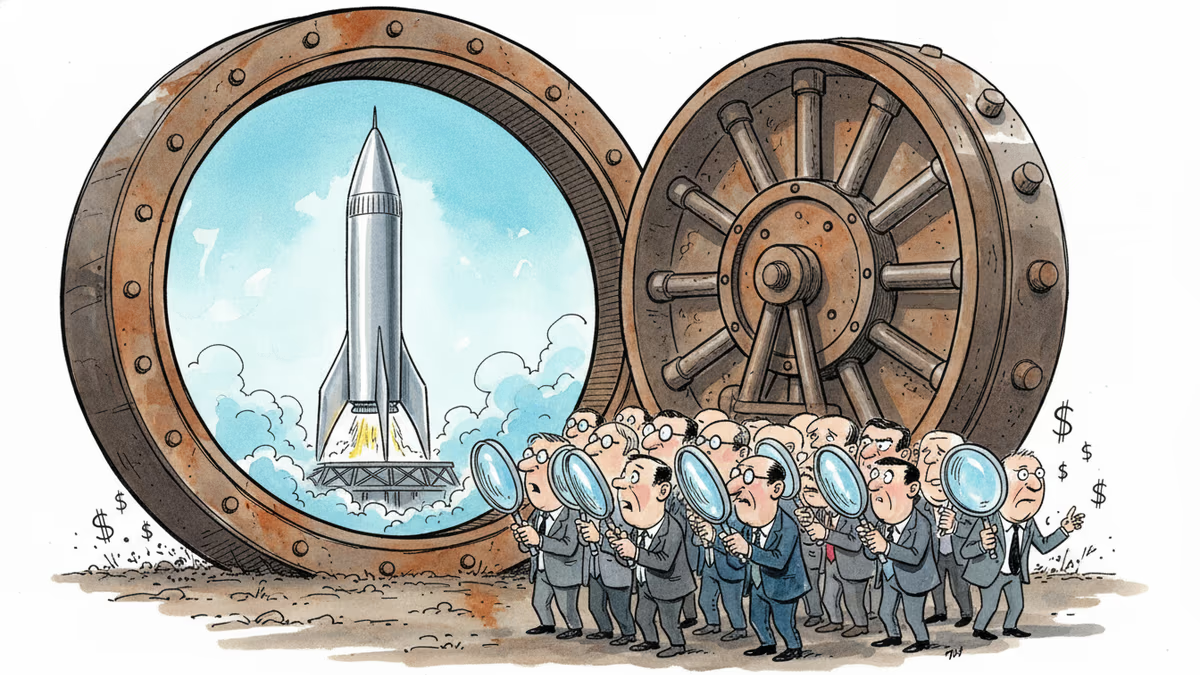

SpaceX Files for IPO—The Numbers Tell Two Stories

SpaceX has filed its S-1 with the SEC, targeting the Nasdaq under ticker SPCX. With $18.67B in revenue but a $4.9B loss, the IPO forces investors to answer one hard question.

$18.67 billion in revenue. $4.9 billion in losses. $20.7 billion in capital expenditures. Pick any one of those numbers and you can build a completely different investment thesis—which is exactly why the SpaceX IPO is going to be one of the most argued-over offerings in recent memory.

SpaceX has officially filed its S-1 prospectus with the SEC, setting up what could be the largest initial public offering ever. The company plans to list on the Nasdaq under the ticker SPCX. For years, getting a piece of Elon Musk's rocket company meant knowing the right venture capitalists. That's about to change.

What the S-1 Actually Says

The headline number is the revenue: $18.67 billion for 2025, a figure that would make most companies the envy of their industry. The more important detail is where that money came from. Starlink, SpaceX's satellite internet service, generated more than $11 billion of it—meaning the rocket launches that made SpaceX famous are, financially speaking, the supporting act.

That's a significant shift. Starlink is a subscription business. It generates recurring revenue, it scales without proportional cost increases, and it operates largely independently of the high-profile, high-risk launch cadence that dominates SpaceX's press coverage. For investors trying to model cash flows, Starlink is the part of the business they can actually underwrite.

The losses are harder to dismiss. The $4.9 billion net loss wasn't a surprise to insiders, but seeing it in a public filing gives it a different weight. More striking is the capex jump—from $11.2 billion in 2024 to $20.7 billion in 2025. That's not a company trimming toward profitability. That's a company betting aggressively that the infrastructure it's building today will generate returns on a timeline it hasn't fully disclosed.

Why Now—And Why This Is Complicated

The timing reflects several converging pressures. Starlink now has enough paying subscribers to demonstrate a repeatable revenue model, which is the baseline requirement for a credible public offering. But the competitive window is narrowing: Amazon's Project Kuiper launched its first production satellites in 2025, and China's state-backed broadband constellation is accelerating. Capital raised now translates directly into satellite deployment speed, and deployment speed is the moat in low-earth-orbit internet.

There's also the Musk factor, which is impossible to separate from the filing. His simultaneous roles as CEO of Tesla, owner of X, founder of xAI, and—until recently—head of the federal government's DOGE initiative create a conflict-of-interest surface area that regulators and institutional investors will scrutinize carefully. SpaceX holds substantial federal contracts with NASA and the Department of Defense. The question of whether those contracts were awarded on merit, and whether a publicly traded SpaceX creates new accountability problems, isn't hypothetical. It's the kind of question the SEC prospectus review process is designed to surface.

Who's Watching, and What They're Thinking

Retail investors are getting something they've never had: direct access to the company that currently dominates commercial launch and is building the infrastructure backbone of satellite internet. The risk is that the story is so compelling it crowds out the math. A company losing nearly $5 billion a year while spending $20.7 billion on capex needs either a dramatic improvement in unit economics or a very long investor time horizon.

Institutional investors will price the offering against a small set of comparables—none of them perfect. Amazon in its early years. Tesla before it turned profitable. Satellite operators like SES and Intelsat, which SpaceX has effectively disrupted. The consensus valuation in private markets has hovered around $350 billion; the public market will render its own verdict.

Competitors face an uncomfortable scenario. A successful IPO gives SpaceX access to public capital markets on an ongoing basis, not just a one-time cash infusion. That changes the competitive math for everyone from Amazon Kuiper to European operator Eutelsat to the emerging Chinese players.

Regulators in Washington and Brussels are watching for different reasons. In the US, the conflict-of-interest questions around Musk's government adjacency are live. In Europe, the debate over dependence on US-controlled satellite infrastructure—sharpened by the war in Ukraine, where Starlink became critical communications infrastructure—gives the IPO a geopolitical dimension that a standard tech listing doesn't carry.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

American Airlines just signed Starlink for 500+ aircraft. It's not just about faster inflight internet — it's a calculated move in the run-up to what could be the largest IPO in history.

SpaceX's upgraded Starship V3 completed its first test flight, deploying 20 Starlink simulators but losing the Super Heavy booster. With an IPO weeks away, the stakes just got higher.

SpaceX's IPO filing puts AI at the center, claiming a $26.5 trillion market opportunity. But can Grok compete with OpenAI and Anthropic for enterprise customers?

SpaceX filed a nearly 400-page S-1 with the SEC, targeting an IPO as early as June 12. Here's what the filing reveals—and what it doesn't.

American Airlines just signed Starlink for 500+ aircraft. It's not just about faster inflight internet — it's a calculated move in the run-up to what could be the largest IPO in history.

SpaceX's upgraded Starship V3 completed its first test flight, deploying 20 Starlink simulators but losing the Super Heavy booster. With an IPO weeks away, the stakes just got higher.

SpaceX's IPO filing puts AI at the center, claiming a $26.5 trillion market opportunity. But can Grok compete with OpenAI and Anthropic for enterprise customers?

SpaceX filed a nearly 400-page S-1 with the SEC, targeting an IPO as early as June 12. Here's what the filing reveals—and what it doesn't.

Thoughts

Share your thoughts on this article

Sign in to join the conversation