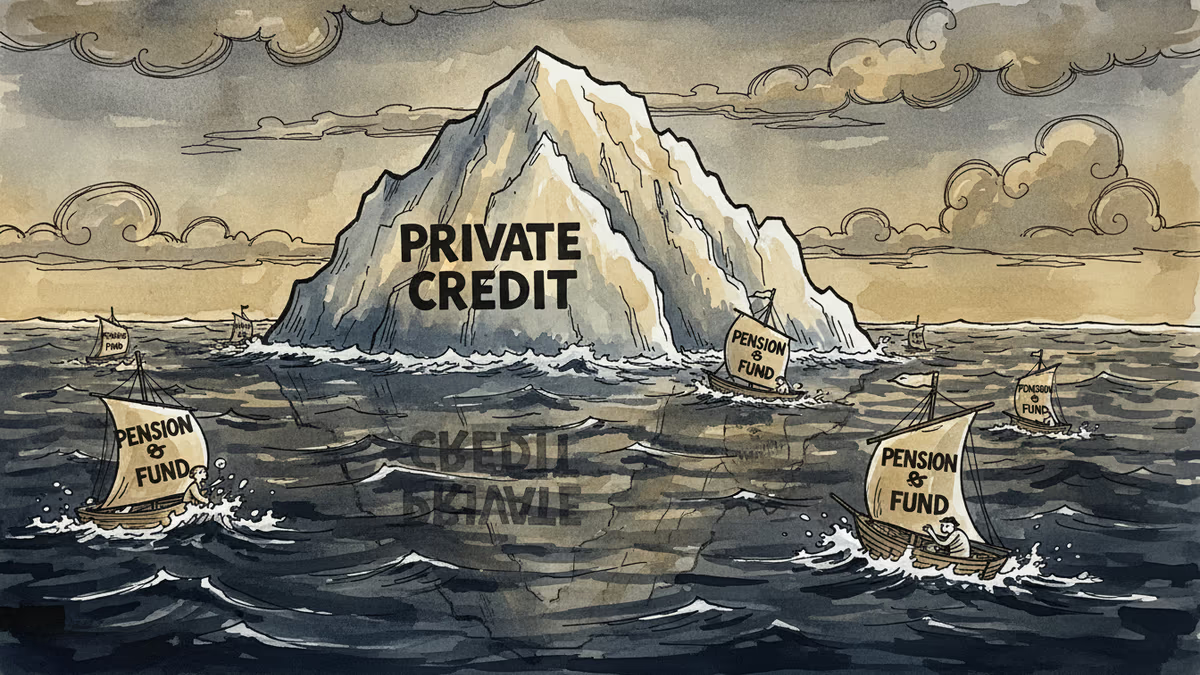

Your Pension Fund's $2 Trillion Shadow Banking Problem

Blue Owl's troubles expose hidden risks in the massive private credit market where pension funds and insurers chase higher yields in an opaque, unregulated space.

Your pension fund is probably invested in a $2 trillion shadow banking system that's showing dangerous cracks. The troubles at Blue Owl Capital, one of America's largest private credit managers, aren't just another Wall Street hiccup—they're a warning sign for an entire industry built on borrowed time.

When the Music Stops

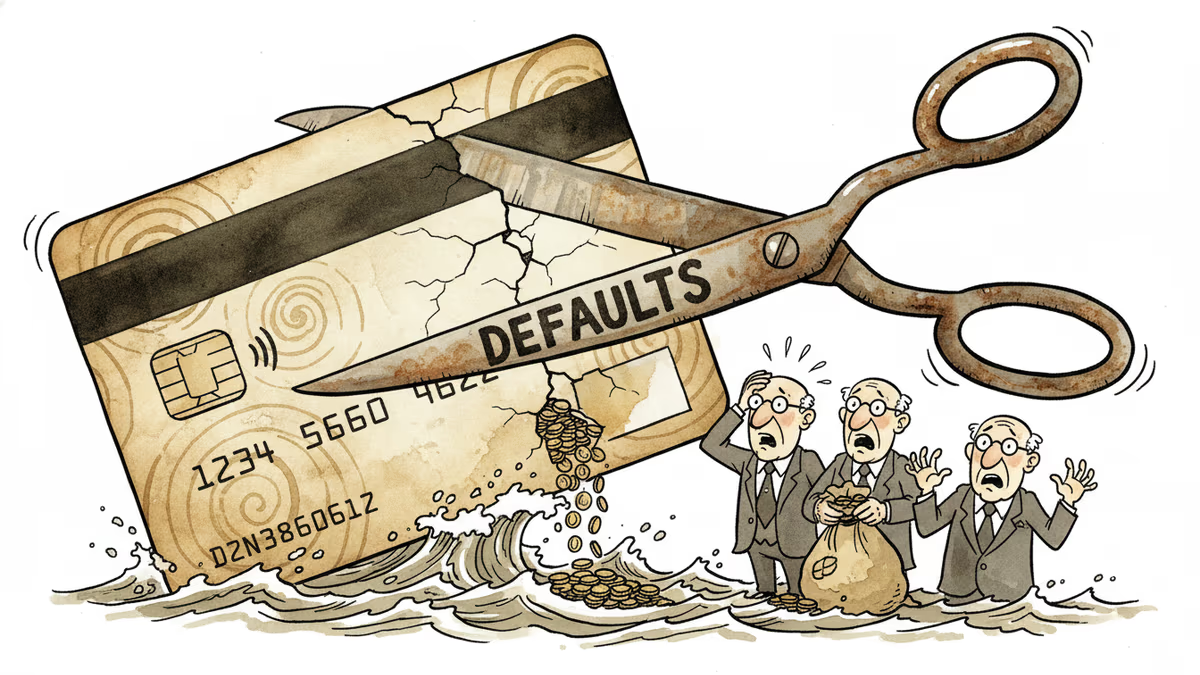

Blue Owl has been hemorrhaging talent and credibility since late last year. Key executives have fled, investment performance has soured, and now liquidity issues are emerging in some of their flagship funds. For a firm managing $174 billion in assets—much of it pension and insurance money—this isn't just corporate drama.

The private credit boom of the last decade was fueled by one simple promise: 8-12% annual returns when traditional bonds barely yielded 2-3%. Pension funds, desperate to meet their obligations to retirees, poured money into this opaque corner of finance. But what happens when the easy money era ends?

The Transparency Black Hole

Here's the uncomfortable truth: nobody really knows what this stuff is worth. Unlike publicly traded bonds, private credit investments don't have daily market prices. Fund managers essentially mark their own homework, valuing assets based on internal models and assumptions.

Blue Owl's problems illustrate this perfectly. While the firm's publicly traded stock has been volatile, the private funds it manages continue to report steady, positive returns. Either they've discovered the secret to defying gravity, or there's a significant lag between reality and reported performance.

Pension fund managers, under pressure to generate returns for millions of retirees, have little choice but to trust these valuations. The alternative—sticking to low-yielding government bonds—means benefit cuts or higher contributions.

Regulators Playing Catch-Up

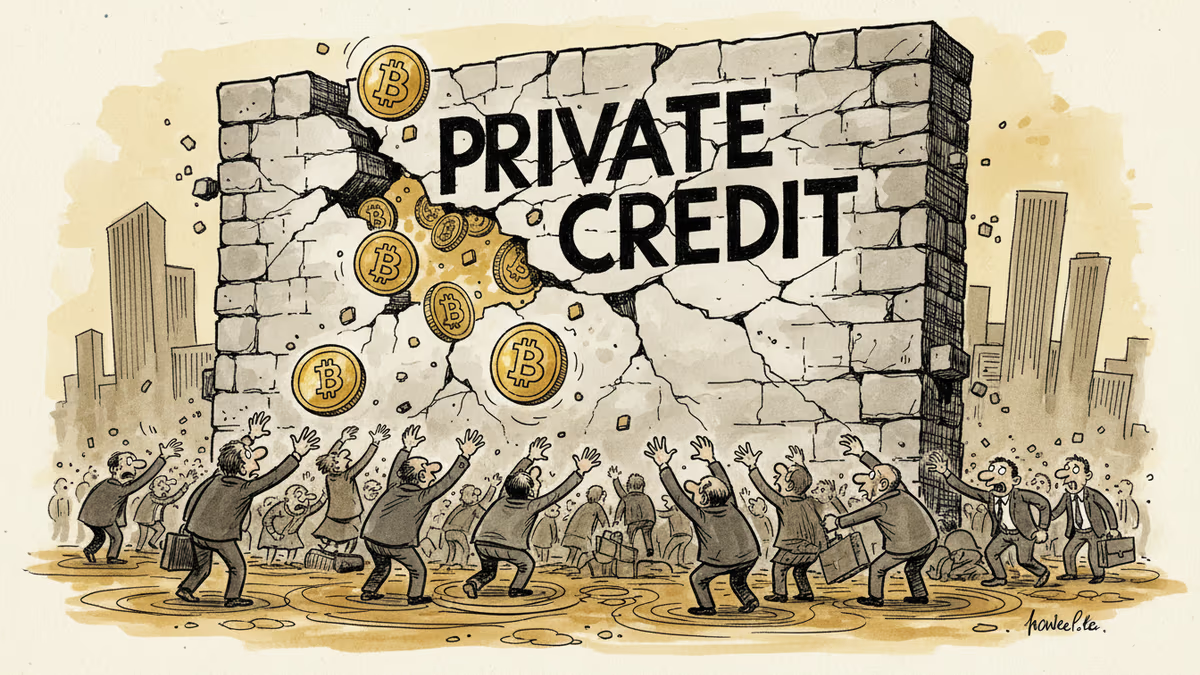

The SEC has been trying to shine more light on private credit, but it's like illuminating a black hole. The industry's entire appeal rests on being "private"—free from the disclosure requirements and market scrutiny that govern public markets.

This creates a regulatory paradox: tighten oversight too much, and the industry migrates offshore or finds new loopholes. Too little, and systemic risks accumulate in the shadows. European regulators are grappling with the same dilemma as private credit grows rapidly across the Atlantic.

The question isn't whether private credit will face a reckoning—it's whether the institutions managing our collective future are prepared for it.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

US private credit default rates reach record highs in 2025, raising concerns for institutional investors including pension funds and insurance companies globally.

BlackRock's $26B private credit fund limits withdrawals as $3.5T market shows cracks. Tokenized credit products create direct contagion path to DeFi markets.

Internal battles at Blue Owl Capital are sending shockwaves through the $1.5 trillion private credit market, raising questions about alternative lending's true risks.

Blue Owl and private credit's explosive growth masks structural risks. Who bears the cost when pension funds chase yield in shadow banking?

US private credit default rates reach record highs in 2025, raising concerns for institutional investors including pension funds and insurance companies globally.

BlackRock's $26B private credit fund limits withdrawals as $3.5T market shows cracks. Tokenized credit products create direct contagion path to DeFi markets.

Internal battles at Blue Owl Capital are sending shockwaves through the $1.5 trillion private credit market, raising questions about alternative lending's true risks.

Blue Owl and private credit's explosive growth masks structural risks. Who bears the cost when pension funds chase yield in shadow banking?

Thoughts

Share your thoughts on this article

Sign in to join the conversation