Oil at $100, Yen at 159: Asia Counts the Cost

Brent crude topped $100 a barrel in Tokyo trading as the yen hit its weakest since January. With Hormuz closure fears mounting, what does this mean for Asian economies and your portfolio?

The last time oil traders watched Brent cross $100, central banks were still fighting post-pandemic inflation. Now it's back—and this time, the fear isn't demand. It's a strait.

What Happened

During Tokyo trading hours on March 12, Brent crude futures breached $100 per barrel. Almost simultaneously, the Japanese yen slid to 159 per dollar—its weakest since mid-January—as investors priced in the likelihood that surging energy costs will blow out Japan's trade deficit.

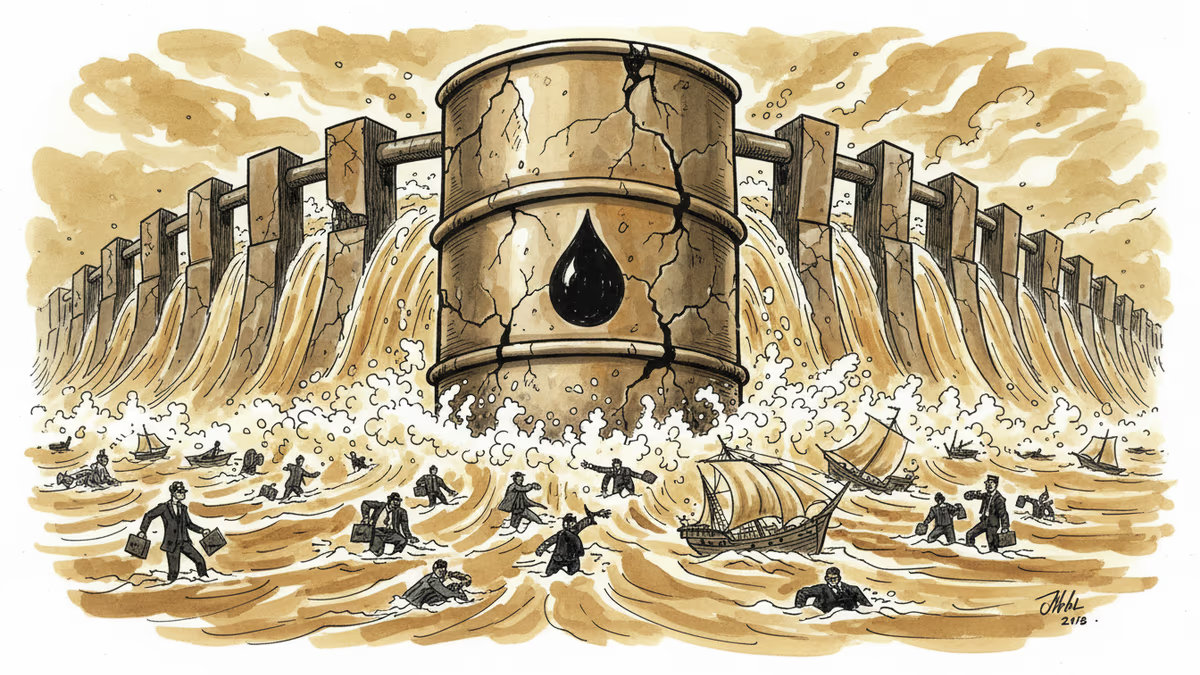

The proximate cause is the intensifying Iran war and the growing investor fear of a prolonged closure of the Strait of Hormuz. Roughly 20% of global seaborne oil passes through that narrow chokepoint. If it closes—even partially, even temporarily—no amount of strategic reserve releases changes the arithmetic.

The IEA announced a record-scale release from member nations' strategic petroleum reserves. Markets shrugged. Asian equities fell sharply. Executives across the region are flagging rising supply chain risks. And investors with exposure to Gulf real estate and equities are reassessing fast.

Why the IEA's Record Release Isn't Working

Strategic reserves exist to buy time, not to replace geography. The IEA's intervention sends a signal: governments are paying attention, and they have ammunition. But the market's logic is blunt—strategic stocks are finite, and a physical blockade of Hormuz cannot be resolved by releasing barrels from tanks in Louisiana or Rotterdam.

What investors are pricing in isn't a short squeeze. It's a scenario where the war drags on for months, where tanker traffic through Hormuz becomes genuinely disrupted, and where alternative supply routes—around the Cape of Good Hope, through pipelines—prove insufficient to cover the gap. At $100, markets are nervous. At $120, they're in crisis mode.

Who Wins, Who Loses

Not everyone is hurting. Japan Steel Works, a supplier of reactor components, has drawn fresh attention as energy security concerns push nuclear power back up the policy agenda across Asia. Shipbuilders with LNG carrier order books are watching their prospects improve. Defense and energy infrastructure companies are quietly benefiting.

The losers are more numerous. Airlines face a direct margin squeeze—fuel typically represents 20–30% of operating costs for major carriers. Petrochemical manufacturers, shipping companies, and any business running energy-intensive logistics are watching their cost assumptions unravel in real time.

For consumers, the transmission is slower but inevitable: higher fuel costs feed into freight, which feeds into food and goods prices. In Japan, the yen depreciation compounds the problem—a weaker currency makes every barrel of imported oil even more expensive in local terms. In South Korea, where oil import dependency exceeds 93%, the math is similarly uncomfortable.

The Hormuz Question Nobody Wants to Answer

Here's the tension at the center of this crisis: the IEA, central banks, and finance ministries can manage market psychology. They cannot manage geography.

The Strait of Hormuz is 33 kilometers wide at its narrowest point. Iran has demonstrated, repeatedly over decades, its willingness to threaten or harass shipping there. The current conflict raises the stakes considerably. And while alternative pipelines exist—Saudi Arabia's East-West Pipeline, the Abu Dhabi Crude Oil Pipeline—their combined capacity falls well short of what Hormuz currently handles.

Taiwan, which has its own acute energy dependence vulnerabilities, is watching closely. So is every Asian economy that has built its industrial base on the assumption of cheap, freely flowing Gulf oil.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

A drone strike on a UAE nuclear power plant sent oil prices up more than 1%. Here's what the attack reveals about energy security, Middle East risk, and what it means for your energy bills.

Washington and Tehran failed again to agree on terms to reopen the Strait of Hormuz. With 20% of global seaborne oil at stake, every day of deadlock has a price—and consumers are paying it.

Tensions over Iran's threat to close the Strait of Hormuz are triggering a surge in precautionary oil buying across Asia and Europe. Here's what's really at stake—and who wins and loses.

Barclays raised its 2026 Brent crude forecast to $100/barrel, citing prolonged Hormuz disruption. Here's what that means for energy markets, inflation, and your energy bill.

A drone strike on a UAE nuclear power plant sent oil prices up more than 1%. Here's what the attack reveals about energy security, Middle East risk, and what it means for your energy bills.

Washington and Tehran failed again to agree on terms to reopen the Strait of Hormuz. With 20% of global seaborne oil at stake, every day of deadlock has a price—and consumers are paying it.

Tensions over Iran's threat to close the Strait of Hormuz are triggering a surge in precautionary oil buying across Asia and Europe. Here's what's really at stake—and who wins and loses.

Barclays raised its 2026 Brent crude forecast to $100/barrel, citing prolonged Hormuz disruption. Here's what that means for energy markets, inflation, and your energy bill.

Thoughts

Share your thoughts on this article

Sign in to join the conversation