The Strait That Moves Markets—and Your Gas Bill

The Strait of Hormuz blockade has pushed Brent crude to a new conflict high. Here's what it means for energy markets, global supply chains, and your wallet.

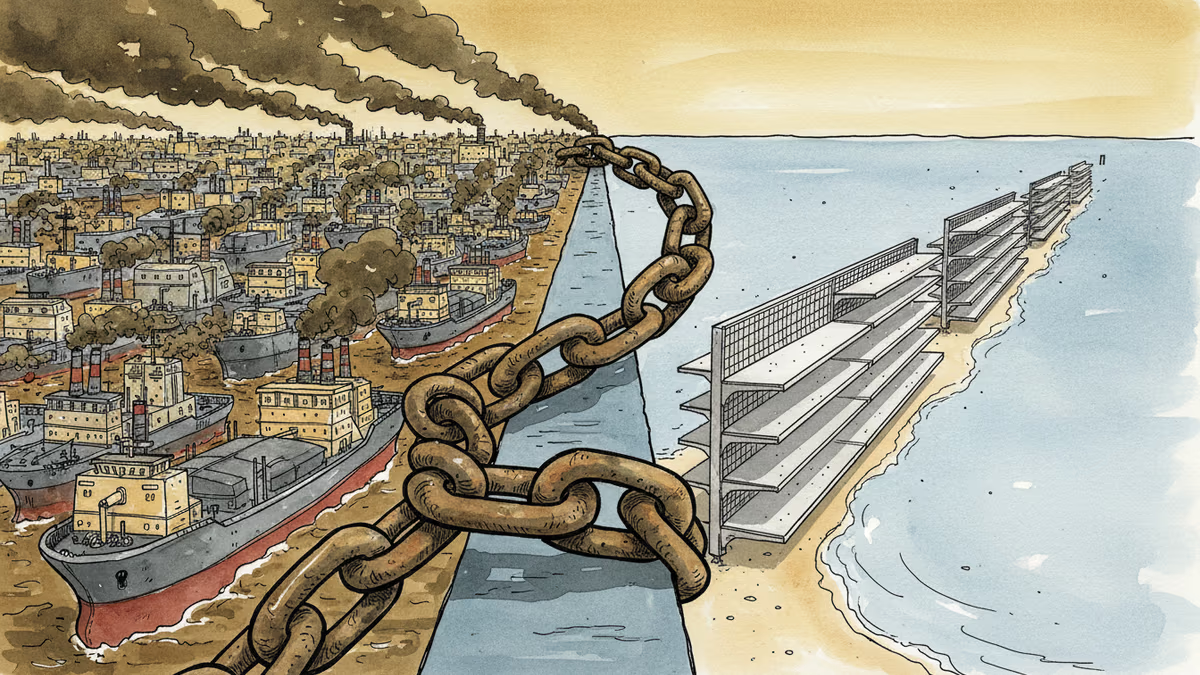

Every barrel of oil that leaves the Persian Gulf has to squeeze through a channel barely 34 kilometers wide at its narrowest point. Right now, that channel is shut.

The Strait of Hormuz blockade has pushed Brent crude to its highest price since the conflict began. That single data point—a new conflict high—is the market's way of saying it no longer believes this is a short-term disruption. It's pricing in something longer, and more expensive.

The Chokepoint That Has No Substitute

The numbers explain why markets are rattled. Roughly 20% of global seaborne oil trade—around 17 million barrels per day—passes through the Strait of Hormuz. Saudi Arabia, Iraq, the UAE, Kuwait, and Iran all funnel their exports through this single corridor. There is no meaningful alternative at scale.

Saudi Arabia's East-West Pipeline offers a partial bypass, but its capacity of roughly 5 million barrels per day covers less than a third of what normally flows through the strait. The math doesn't work. When the chokepoint closes, the oil doesn't reroute—it just stops.

Beyond crude, the blockade is squeezing liquefied natural gas shipments from Qatar, one of the world's largest LNG exporters. Europe, which has spent the past three years diversifying away from Russian gas, now finds one of its key alternative suppliers cut off.

Winners, Losers, and What It Costs You

The beneficiaries of this crisis are easy to identify. U.S. shale producers in the Permian Basin are insulated from Hormuz entirely. Higher global prices mean fatter margins without any change in their operations. Norway, Canada, and other non-Gulf producers are in the same position—their oil just became more valuable overnight.

The losers are more numerous. Asian importers—Japan, South Korea, India, China—collectively absorb the majority of Persian Gulf exports. For these economies, there is no quick pivot. Refineries are built around specific crude grades; you can't simply swap in West Texas Intermediate for Arab Heavy on short notice.

For the average consumer, the transmission mechanism is straightforward. A $10 per barrel increase in Brent crude typically adds $0.08–$0.10 to a gallon of gasoline in the U.S. over several weeks. Jet fuel tracks crude closely, meaning airline tickets will follow. Petrochemicals—plastics, fertilizers, synthetic materials—will feel the pressure too, working their way into prices across supply chains over months, not days.

Strategic Petroleum Reserve releases can blunt the immediate shock. IEA member countries have coordinated releases before, most recently in 2022 following Russia's invasion of Ukraine. But reserves are finite, and the U.S. SPR is at historically low levels after successive drawdowns. A sustained blockade tests the limits of that buffer.

Why This Time Feels Different

Hormuz has been threatened before. The Iran-Iraq War of the 1980s produced the "Tanker War," with both sides attacking shipping in the Gulf. The strait survived. But context matters.

This isn't a threat—it's an active blockade. The gap between futures prices and spot prices is narrowing, a technical signal that traders are pricing in immediate supply shortfall rather than future risk. War risk insurance premiums for vessels in the region have spiked, adding cost even for ships that aren't directly affected.

Geopolitical resolution timelines are opaque. Diplomatic back-channels may be working; they may not be. Military escalation remains a live variable. Markets hate uncertainty more than bad news, and right now they have both.

There is also a structural dimension that wasn't present in previous Hormuz crises. The global energy transition has created a paradox: investment in new fossil fuel production has slowed under ESG pressure, even as the world hasn't yet built enough renewable capacity to compensate. Spare capacity in OPEC+ is tighter than it appears on paper. The buffer the world relied on in past crises is thinner.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

Ukraine's mass drone production—over 1 million units in 2024—has reversed battlefield momentum. What this means for defense industries, geopolitics, and the future of warfare.

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Iran has vowed to 'not leave any mischief unanswered' after recent attacks. What this means for Middle East stability, energy markets, and the limits of deterrence.

Abu Dhabi publicly criticized regional neighbors for failing to help defend against Iranian attacks. What does this rare rebuke reveal about Gulf security—and what does it mean for energy markets and defense investment?

Ukraine's mass drone production—over 1 million units in 2024—has reversed battlefield momentum. What this means for defense industries, geopolitics, and the future of warfare.

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Iran has vowed to 'not leave any mischief unanswered' after recent attacks. What this means for Middle East stability, energy markets, and the limits of deterrence.

Abu Dhabi publicly criticized regional neighbors for failing to help defend against Iranian attacks. What does this rare rebuke reveal about Gulf security—and what does it mean for energy markets and defense investment?

Thoughts

Share your thoughts on this article

Sign in to join the conversation