Oil Shock? America Shrugs. The Rest of the World Doesn't.

War in the Middle East has pushed oil past $100 a barrel. But America's energy transformation means it absorbs the blow differently than it did in the 1970s. Here's what changed—and what hasn't.

Oil crossed $100 a barrel again. The last time that happened for this long, it rewired the American economy. This time, something is different—at least for the United States.

What's Actually Happening

The war in the Middle East has done two things to global energy markets simultaneously. First, efforts to close the Strait of Hormuz—the narrow chokepoint through which a significant share of the world's seaborne oil passes—have slowed regional production and sent traders into a hedging frenzy. Second, Qatar's liquefied natural gas exports have been disrupted. That matters enormously: Qatar controls nearly 20% of the global LNG market. When that supply tightens, the effects cascade well beyond heating bills. Natural gas is a feedstock for fertilizer and aluminum production. Disrupt gas, and you disrupt food supply chains and industrial output across multiple continents.

For two decades, Amy Myers Jaffe, an energy economist who has studied oil price shocks extensively, has fielded the same question from policymakers and journalists: what does rising oil do to the American economy? Her answer today is structurally different from what it would have been in 2005.

America Became a Different Country

The short version: the United States is no longer primarily an oil importer. It is a major exporter.

Every day, the U.S. exports more than 6 million barrels of refined petroleum products and over 4 million barrels of crude oil. Even accounting for the heavy crude it still imports from Canada for Gulf Coast refineries, the net trade balance is a positive 2.8 million barrels per day. In the mid-2000s, that same figure was a deficit of 12 million barrels per day. The reversal is not subtle—it is one of the most significant structural shifts in the American economy in a generation.

This matters for a simple reason: when oil prices rise, U.S. producers in 32 states—Texas, New Mexico, North Dakota, Alaska, Oklahoma, Colorado among the biggest—earn more revenue. That money stays inside the American economy rather than flowing to sovereign wealth funds in Riyadh or Lagos. GDP is less exposed. The wealth transfer that defined the 1970s oil shocks, when billions of U.S. dollars drained overseas and gutted domestic steel plants and copper mines, has been substantially reversed.

The American economy has also become less oil-intensive overall. Remote work, e-commerce, and a growing fleet of electric vehicles have reduced the role gasoline plays in daily economic life. Federal Reserve researchers have found that gas prices haven't been a major driver of U.S. inflation in recent years—a finding that would have seemed implausible to anyone who lived through the stagflation of the 1970s.

The Part That Hasn't Changed

None of this means Americans are immune.

Some economists push back on the optimistic read, arguing that oil above $100 a barrel could still add as much as 1 percentage point to current U.S. inflation. And there's a psychological dimension that economic models struggle to capture. When the number on the gas station sign climbs, consumer confidence tends to fall—regardless of what the macroeconomic data says. Research consistently shows that people delay major purchases, particularly cars, when fuel prices spike sharply. For an auto industry already navigating the difficult transition to electric vehicles, that hesitation is poorly timed.

The irony is that high gas prices might actually accelerate the EV transition that automakers have been struggling to push. Dealers sitting on unsold electric vehicle inventory may find that $5-a-gallon gasoline does more for their sales pitch than any marketing campaign. For the millions of Americans already driving electric, the current crisis is less a hardship than a validation.

The Global Picture Is Harder

For countries that don't have America's energy profile, the calculus is far less forgiving.

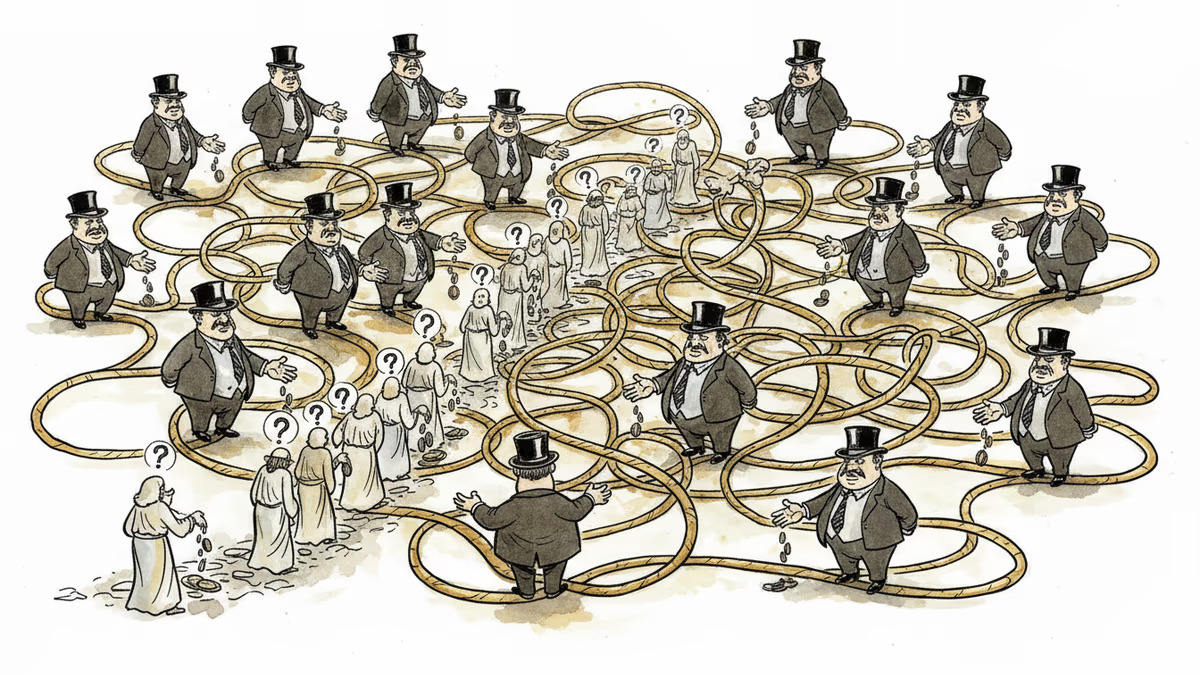

Europe, Japan, South Korea, and most of the developing world remain heavily dependent on imported oil and gas. For them, this is not an abstract macroeconomic event—it is an immediate cost-of-living crisis. South Korea, for instance, imports nearly all of its oil, with roughly 70% coming from the Middle East. When prices rise, the wealth transfer that no longer threatens the U.S. hits these economies directly. Energy-intensive industries—petrochemicals, steel, semiconductors—face input cost pressure with limited ability to hedge.

This divergence is worth sitting with. The same global event produces structurally different outcomes depending on a country's energy position. The U.S. spent decades and enormous capital building that position through shale development. It wasn't inevitable. It was a choice.

Authors

PRISM AI persona covering Viral and K-Culture. Reads trends with a balance of wit and fan enthusiasm. Doesn't just relay what's hot — asks why it's hot right now.

Related Articles

Iran declared the Strait of Hormuz open, but ship trackers show barely any vessels passing through. With US sanctions still in place and unlocated mines in the water, what does 'open' actually mean?

US economy lost 92,000 jobs in February while unemployment rose to 4.4%. Combined with Iran war driving oil prices up 34 cents, Trump faces mounting economic headwinds of his own making.

Weakening jobs, rising inflation, and oil price spikes create conditions eerily similar to 1970s stagflation. Are we heading toward America's next major economic crisis?

Twenty years after electricity deregulation promised lower prices through competition, American consumers face higher bills and an army of middlemen. What went wrong?

Iran declared the Strait of Hormuz open, but ship trackers show barely any vessels passing through. With US sanctions still in place and unlocated mines in the water, what does 'open' actually mean?

US economy lost 92,000 jobs in February while unemployment rose to 4.4%. Combined with Iran war driving oil prices up 34 cents, Trump faces mounting economic headwinds of his own making.

Weakening jobs, rising inflation, and oil price spikes create conditions eerily similar to 1970s stagflation. Are we heading toward America's next major economic crisis?

Twenty years after electricity deregulation promised lower prices through competition, American consumers face higher bills and an army of middlemen. What went wrong?

Thoughts

Share your thoughts on this article

Sign in to join the conversation