Rivals Caught Nvidia's Chips. So Why Won't Its Share Move? The Moat Is CUDA

AMD's MI325X matches or beats Nvidia on memory and bandwidth — yet Nvidia's 86-92% share holds. The real moat is CUDA, 20 years in the making. Part 1 of 4.

Rivals Caught Nvidia's Chips. So Why Won't Its Share Move? The Moat Is CUDA

A faster chip arrived. The market didn't flinch.

Last year, AMD unveiled its new AI accelerator, the MI325X, leading with 256GB of memory and 6 terabytes per second of bandwidth — numbers that top the memory capacity of Nvidia's flagship parts (per AMD's own spec sheet). And yet, across the 2024 global market for data-center AI accelerators, Nvidia's share is estimated at 86-92% (Mercury Research and multiple analyst citations). On the spec sheet, Nvidia lost ground. In the market, it didn't lose a thing.

This is Part 1 of PRISM's series, Semiconductor Sovereignty. The question here is simple: when rivals ship a better chip, why doesn't Nvidia's share budge? The short answer is that the contest isn't being decided on the silicon.

On paper, it's already a close race

Chip for chip, Nvidia's commanding lead doesn't add up.

AMD's MI300X shipped with 192GB of memory and 5.3TB/s of bandwidth, edging past the memory capacity of Nvidia's H100 and H200. The follow-up MI325X pushed further still. Google, meanwhile, designed its in-house TPU v6e (Trillium) around power efficiency, and it's rated to draw less power than the H100's 700W (Nvidia's published spec). One caveat: the frequently cited "TPU 300W" figure isn't clearly confirmed as an official Google TDP, so it's safest to treat it as a reference point rather than a hard number.

| Chip | Memory | Bandwidth | Notable for |

|---|---|---|---|

| AMD MI300X | 192GB HBM3 | 5.3TB/s | Exceeds H100/H200 memory capacity |

| AMD MI325X | 256GB HBM3e | 6TB/s | On par or ahead on memory and bandwidth |

| Google TPU v6e | Custom design | Custom design | ~300W est. (H100 draws 700W) |

The performance gap has narrowed too. AMD reported that an eight-way MI325X configuration came within 3-7% of Nvidia's H200 on Llama 2-70B inference (results submitted to MLPerf Inference v5.0, April 2025, via AMD's ROCm blog). These are vendor-submitted numbers, so they shouldn't be taken at face value — but on hardware alone, this is no longer the kind of gap you'd call insurmountable.

Here's the paradox. On memory, on bandwidth, on power efficiency, rivals are level or ahead. And the money still flows to Nvidia. The company's data-center revenue came in around $115 billion, up roughly 142% year over year (per Nvidia's fiscal 2025 results). A dead heat on specs and a runaway on revenue, happening at the same time.

A new engine, but no roads to drive it

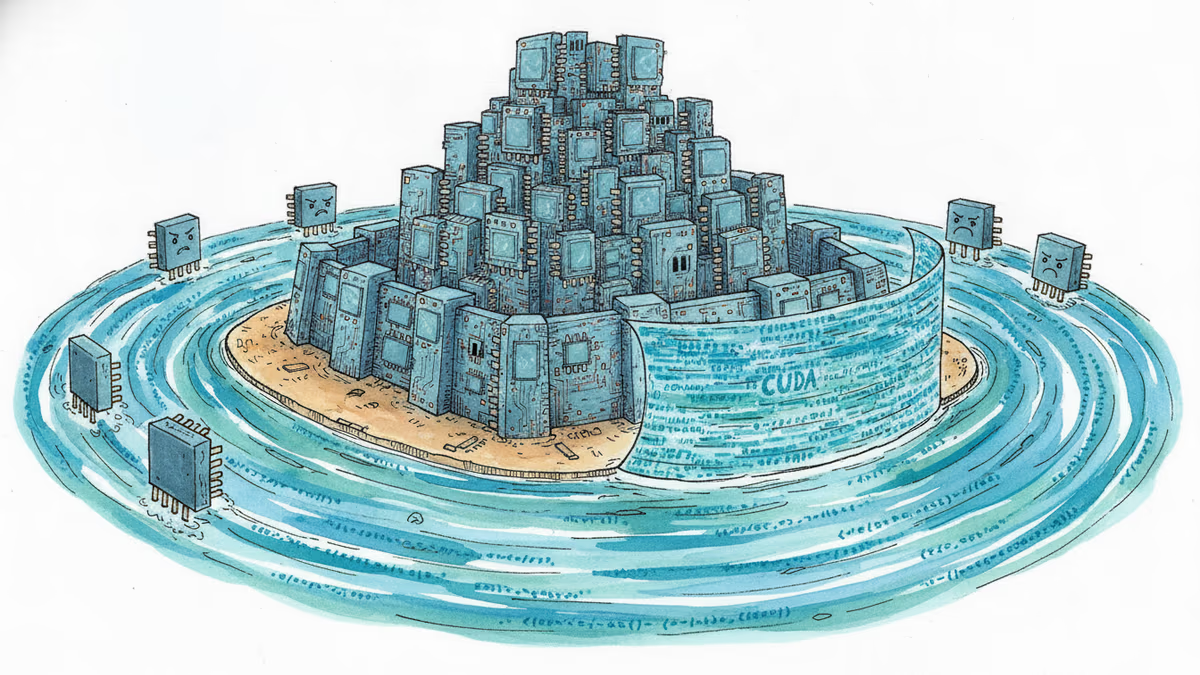

The key to the paradox is CUDA.

CUDA is the software platform Nvidia introduced as an architecture in 2006 and opened up as a developer toolkit in 2007 — nearly 20 years of accumulation. By Nvidia's own count, it now has roughly 6 million developers, with more than 900 CUDA-X libraries stacked on top (NVIDIA GTC 2025 keynote). That developer figure isn't a single snapshot; it's a running total that has climbed year after year — from an estimated 4 million in older industry analyses, to 5 million at GTC 2024, to 6 million at GTC 2025. It's better read as the result of two decades of buildup than as a headcount at any one moment.

Think of it this way. A new chip is a faster engine. CUDA is the entire road network that engine has to drive on. A fast engine goes nowhere without roads.

That road network is a stack of libraries: cuDNN for deep-learning operations, cuBLAS for linear algebra, NCCL for communication across multiple GPUs, TensorRT for inference optimization, layer upon layer. Each is the product of years of tuning baked in over time. You'll see the scale described as "thousands of engineer-years," though that's an industry-blog estimate rather than an official figure. Developers just reach for these and use them. They don't rebuild from scratch. In investor circles, this is exactly why Nvidia gets described less as a chipmaker than as a software platform that happens to sell hardware.

The catch is that this code doesn't just run on a competitor's chip. Moving to a different accelerator means rewriting a large share of production code, revalidating it, and retraining the team. In PRISM's analysis, that porting cost generally outweighs whatever performance gain a new chip delivers. So customers run the math and stay with Nvidia.

Testimony from the field shows how high the wall really is. Park Jung-ho, vice chairman of SK Hynix — the memory giant that supplies HBM to Nvidia — said every AI-chip engineer he hires asks for the same thing: let me work with Nvidia GPUs and CUDA. Ask them to build on a domestic chip instead, he said, and it takes three times as long or more (Kyunghyang Shinmun, March 2024). At Rebellions and FuriosaAI, two of Korea's homegrown AI-chip startups, software engineers reportedly make up 40-50% of the staff (Unicorn Factory's "Behind Chips," June 2025). These are companies that build chips, and half their people are wrestling with software. That number tells you where the real fight is.

A legitimate payoff, or a bottleneck on innovation?

The same phenomenon draws exactly opposite verdicts.

Nvidia and its defenders see it as the fair reward for investment. CUDA is the result of 20 years and thousands of engineer-years, they argue, and it bundles more than raw performance: developer experience, stability, documentation, community. CEO Jensen Huang has consistently framed CUDA not as hardware but as a "flywheel" and a platform that keeps accelerated computing turning (GTC 2025 and 2026 keynotes, paraphrased). By this logic, an ecosystem two decades in the making is itself a legitimate part of the product's value — and customers have no reason to take on porting risk when a proven stack is right there.

Challengers and the open camp read it differently. Proprietary lock-in, they say, hands Nvidia pricing power and creates supply dependence, which in turn drags on AI costs and the pace of innovation. "Plenty of GPUs, but only one CUDA" captures the worry in a phrase (ZDNet Korea, August 2025). This camp points to the history of computing, where open standards have repeatedly displaced closed stacks. Whether that ending repeats this time, though, no one can yet call.

Along the time axis, the picture sharpens a little. Back in 2006-2007, when most people still saw GPUs as gaming hardware, Nvidia was seeding CUDA among academics and researchers — driving in a "wedge," as Japan's Nikkei put it. When the AI boom arrived, that wedge had grown into a moat. Right now is peak defensibility.

Cracks and durability, at the same time

None of this means the moat lasts forever.

Analysts project that Nvidia's share of data-center AI accelerators could slip to around 75% by 2026 (Mercury Research and Bernstein forecasts, per reporting) — a number that reflects more competing chips and the push by large clouds like Google and Amazon toward their own silicon. But a falling share can coexist with rising absolute revenue, because the market itself keeps expanding. This is a stretch where "trouble" and "record results" hold true at once.

China is a different board entirely. Under export controls, Nvidia's share inside China is reported to have fallen from roughly 90-95% at one point to around 54-55% in 2025 (Bernstein and Taiwanese outlets, with wide variance across sources). Jensen Huang has gone as far as to say the company went "from 95% to zero" in China (multiple reports). But that plunge is a special case created by regulation, and mixing it into the global trend line leads readers astray. These two figures have to be read separately.

The series ahead

That's the setup for Part 1: why hardware alone can't win — because the moat lives in software.

So how does a wall like this get breached? The counterattack comes on three fronts. Part 2 looks at the push from open standards and the RISC-V camp — the movement toward open software stacks built to strip out vendor dependence. Part 3 turns to China's drive for domestic chips, accelerating under export controls. Part 4 takes on the regulatory battleground, where policy moves market share directly.

Two facts stand out from this installment. All three counterattacks aim at the same terrain — software standards and the regulatory landscape. And whether any of them succeeds, no one can yet say for certain.

One thing is clear. Building a faster chip, on its own, won't route around this road network. Who rewrites that calculation first — that's the story of the next three parts.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

Snowflake's new $6 billion AWS contract is about more than cloud spending. It signals a shift in AI infrastructure—away from Nvidia GPUs and toward cheaper, homegrown chips for the agent era.

Beijing added an Nvidia gaming chip to its customs ban list the same week Jensen Huang visited China with Trump. Here's what it means for the chip war—and who actually wins.

SpaceX plans to invest at least $55 billion in a Texas AI chip factory called Terafab, with total costs potentially reaching $119 billion. We break down what's real, what's at stake, and who wins or loses.

Cerebras Systems is targeting a $26.6B valuation in what could be 2026's largest tech IPO. But the real story is how deeply OpenAI is embedded in its capital structure—as customer, lender, and potential shareholder.

Snowflake's new $6 billion AWS contract is about more than cloud spending. It signals a shift in AI infrastructure—away from Nvidia GPUs and toward cheaper, homegrown chips for the agent era.

Beijing added an Nvidia gaming chip to its customs ban list the same week Jensen Huang visited China with Trump. Here's what it means for the chip war—and who actually wins.

SpaceX plans to invest at least $55 billion in a Texas AI chip factory called Terafab, with total costs potentially reaching $119 billion. We break down what's real, what's at stake, and who wins or loses.

Cerebras Systems is targeting a $26.6B valuation in what could be 2026's largest tech IPO. But the real story is how deeply OpenAI is embedded in its capital structure—as customer, lender, and potential shareholder.

Thoughts

Share your thoughts on this article

Sign in to join the conversation