Europe and Asia Are Fighting Over the Same LNG Tankers

Iran's war is squeezing LNG supply through the Strait of Hormuz, forcing Europe and Asia into a direct bidding war. Here's who wins, who loses, and what it means for energy prices.

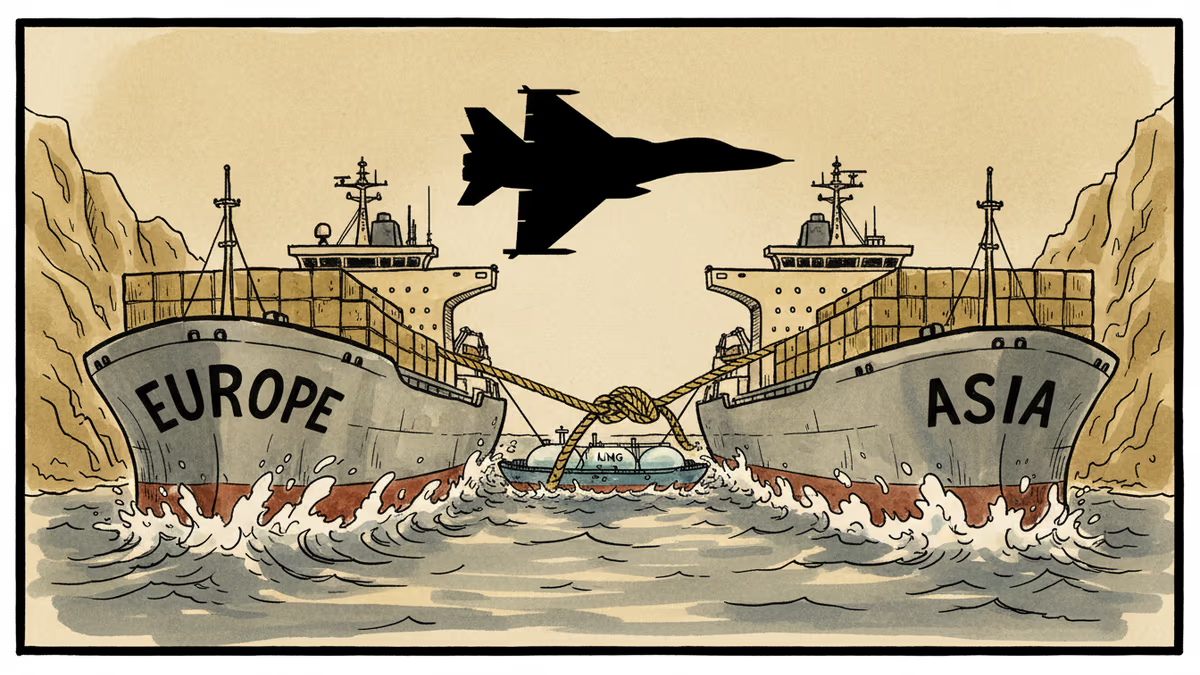

One war. One chokepoint. Two continents scrambling for the same gas.

The conflict involving Iran has done what energy analysts long feared: it's turned the Strait of Hormuz into a liability, and suddenly Europe and Asia are no longer buying from different shelves — they're fighting over the same inventory.

What's Actually Happening

The Strait of Hormuz is the world's single most important energy corridor. Roughly 20% of all LNG traded globally passes through it, most of that originating from Qatar — the world's largest LNG exporter. As conflict risks in the region have escalated, shipping companies have begun rerouting or delaying transits, driving up freight costs and compressing effective supply.

The knock-on effect is immediate. Asian spot LNG prices, measured by the Japan Korea Marker (JKM), have climbed sharply in recent weeks. European buyers, already conditioned by the Russia gas crisis of 2022 to pay almost anything for supply security, are now competing directly with Asian utilities for Atlantic-basin and spot cargoes. The result: a global LNG market that was beginning to loosen is tightening again, faster than most traders expected.

Two Very Different Buyers, One Shrinking Pool

Europe and Asia approach this crisis from fundamentally different positions — and that shapes how each will respond.

Europe has spent the past three years rewiring its energy infrastructure after cutting Russian pipeline gas. LNG import terminals have been built at speed across Germany, Italy, and the Netherlands. For European policymakers, energy security is now a political imperative that overrides price sensitivity. They will pay the premium.

Asia — particularly Japan, South Korea, and Taiwan — has traditionally locked in supply through long-term contracts precisely to avoid this kind of exposure. But those contracts don't cover every scenario, and spot purchases remain a critical buffer during demand spikes or unexpected outages. When spot prices surge, that buffer becomes expensive.

| Factor | Europe | Asia (Japan/Korea/Taiwan) |

|---|---|---|

| Primary suppliers | Qatar, US, Norway | Qatar, Australia, US |

| Hormuz exposure | Moderate | High |

| Price sensitivity | Low (security first) | High |

| Spot market reliance | Growing | Structural buffer |

| Strategic response | More US LNG contracts | Australia + US diversification |

| Political urgency | Acute | Rising |

The One Clear Winner: American LNG

While Europe and Asia compete, US LNG exporters are watching their order books fill. Gulf Coast LNG carries zero Hormuz risk, and the Trump administration has been aggressively promoting export expansion — both as an economic play and a geopolitical tool. For Cheniere Energy, Venture Global, and others, this crisis is a sales pitch they didn't have to write.

The US has gone from a marginal LNG exporter a decade ago to the world's largest in 2023, shipping roughly 90 million tonnes annually. That position only strengthens when Middle Eastern supply becomes unreliable. Washington understands this, and is leveraging it.

The Deeper Problem: Pricing in Geopolitical Risk

What this crisis reveals isn't just a supply shortage — it's a structural mispricing that has persisted for years. LNG contracts and infrastructure investments have long been made on the assumption that the Hormuz Strait would remain functionally open. That assumption is now being stress-tested in real time.

The energy industry will adapt: more long-term contracts away from the Gulf, faster buildout of alternative supply routes, renewed interest in Australian and Canadian LNG projects. But adaptation takes years and capital. In the short term, the cost of this mispricing lands on consumers and utilities — in the form of higher electricity bills, industrial energy costs, and, in some cases, government deficits where regulators have capped retail prices.

For energy traders, the volatility creates opportunity. For policymakers, it creates pressure. For households, it creates bills.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Ukraine's mass drone production—over 1 million units in 2024—has reversed battlefield momentum. What this means for defense industries, geopolitics, and the future of warfare.

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Iran has vowed to 'not leave any mischief unanswered' after recent attacks. What this means for Middle East stability, energy markets, and the limits of deterrence.

Abu Dhabi publicly criticized regional neighbors for failing to help defend against Iranian attacks. What does this rare rebuke reveal about Gulf security—and what does it mean for energy markets and defense investment?

Ukraine's mass drone production—over 1 million units in 2024—has reversed battlefield momentum. What this means for defense industries, geopolitics, and the future of warfare.

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Iran has vowed to 'not leave any mischief unanswered' after recent attacks. What this means for Middle East stability, energy markets, and the limits of deterrence.

Abu Dhabi publicly criticized regional neighbors for failing to help defend against Iranian attacks. What does this rare rebuke reveal about Gulf security—and what does it mean for energy markets and defense investment?

Thoughts

Share your thoughts on this article

Sign in to join the conversation