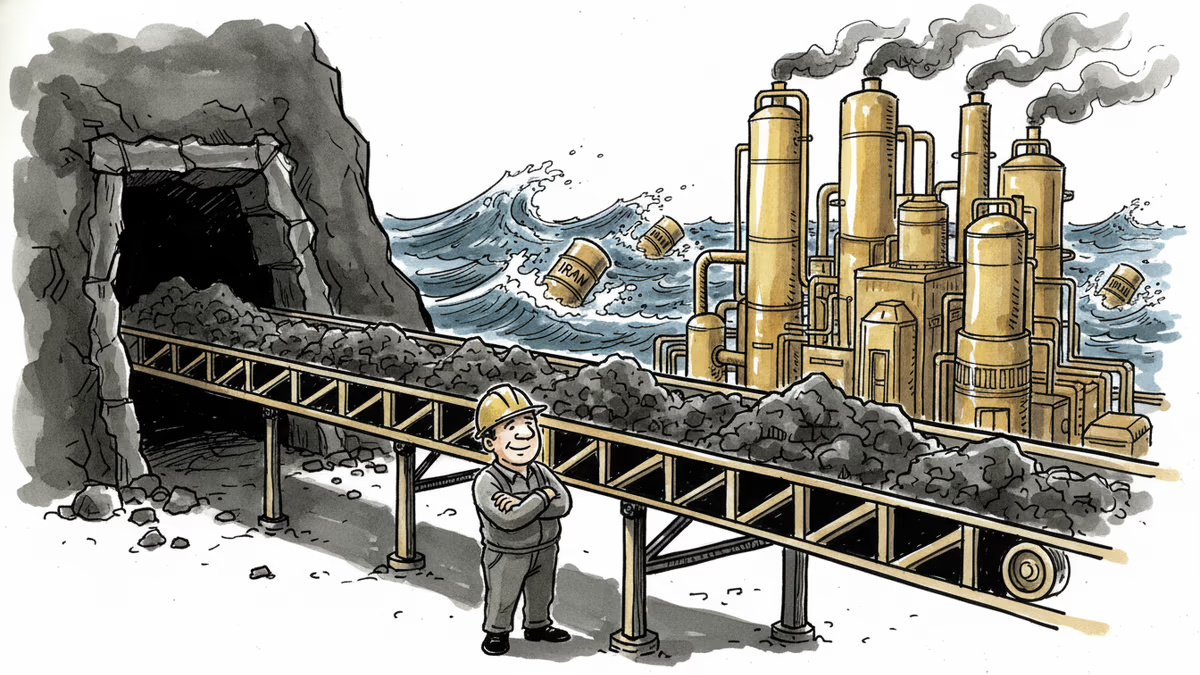

Coal Fills the Gap as Iran War Rattles Oil Markets

As the Iran war disrupts global oil and chemical supplies, China's coal-chemical industry in Xinjiang is moving fast to fill the void. A ground-level look at the opportunity—and its contradictions.

While the Iran war sends oil prices lurching and chemical supply chains into disarray, a very different kind of energy calculation is playing out on the salt flats of northern Xinjiang.

The Plant That Doesn't Need Oil

It was late April in the Changji Hui Autonomous Prefecture, and the heat was already brutal. But the activity on the ground had nothing to do with the season. Trucks running in shifts, expansion construction at full tilt, smokestacks working overtime. This is one of China's four designated large-scale coal-chemical production bases—and right now, it's running like it has somewhere to be.

The logic isn't complicated. As the Iran war throttles global oil and petrochemical output, China is betting that coal-derived chemicals can absorb the slack. Coal-to-chemicals technology—converting coal into plastics feedstocks, fertilizers, synthetic fibers, and fuels—is something Beijing has spent decades and enormous capital developing. That investment is now paying off in ways the planners may not have fully anticipated.

The process works by gasifying coal into a synthesis gas, which is then converted into a range of chemical products that industry would normally derive from crude oil or natural gas. It's not new science. Germany used it in World War II. South Africa's Sasol built a coal-chemicals empire during apartheid-era sanctions. What's new is the scale China has achieved—and the geopolitical moment that's suddenly made it relevant to the whole world.

A Strategic Bet Decades in the Making

China sits on the world's third-largest coal reserves but imports a substantial share of its oil. Every time the Middle East destabilizes, that dependency becomes a strategic liability. Coal chemicals were always partly about hedging that risk—a long-term insurance policy against exactly the kind of supply shock now unfolding.

Xinjiang fits the strategy almost perfectly: abundant coal, cheaper land, and consistent central government backing. The Changji region has grown into both a testing ground and a production hub, churning out olefins, ethanol, and urea fertilizer at scales that increasingly matter beyond China's borders.

The Iran war has shifted the frame. What was once a domestic substitution play is now positioning itself as a global supply alternative. That's a meaningful escalation—and it's happening fast.

The Contradictions Are Hard to Ignore

But this isn't a clean story of industrial triumph. Coal-to-chemicals processes are significantly more carbon-intensive than their petroleum-based equivalents—by some industry estimates, producing several times more CO₂ per unit of output. China has committed to carbon neutrality by 2060. Scaling up coal chemicals now creates a tension that Beijing hasn't publicly resolved.

Then there's Xinjiang itself. The region is already under sustained scrutiny for its treatment of the Uyghur population. The U.S. Uyghur Forced Labor Prevention Act (UFLPA) establishes a rebuttable presumption that goods from Xinjiang are made with forced labor, effectively barring them from American markets. The EU is tightening similar frameworks. For any global company considering sourcing chemicals that trace back to this supply chain, the compliance exposure is real and growing.

From Beijing's vantage point, these objections look like geopolitical pressure dressed up as ethics—an attempt to neutralize a competitive advantage at the moment it becomes most useful. The Iran war, paradoxically, has strengthened China's internal argument for energy self-reliance, making the coal-chemicals push easier to justify domestically even as it draws more scrutiny abroad.

For energy-sector investors and procurement professionals, the picture is genuinely complicated. The supply is real, the scale is real, and the price may be competitive. But the regulatory and reputational risks attached to Xinjiang-origin products are not going away—and in some markets, they're getting worse.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

Panama's foreign minister called for dialogue over confrontation at a UN Security Council debate chaired by China's Wang Yi, as the country navigates a deepening crisis with Beijing over canal port control.

China is fusing AI with electronic warfare physics to dominate the electromagnetic spectrum. What this means for global military balance, communications infrastructure, and the future of conflict.

Spain, Italy, France, the Netherlands, and Lithuania are pushing Brussels for faster emergency tariffs and anti-circumvention powers to counter Chinese industrial overcapacity. Here's what's at stake.

Trump says a US-Iran nuclear deal is 'largely negotiated.' Iran calls it a 'Persian-style peace.' Both sides claim victory. Here's what's actually at stake.

Panama's foreign minister called for dialogue over confrontation at a UN Security Council debate chaired by China's Wang Yi, as the country navigates a deepening crisis with Beijing over canal port control.

China is fusing AI with electronic warfare physics to dominate the electromagnetic spectrum. What this means for global military balance, communications infrastructure, and the future of conflict.

Spain, Italy, France, the Netherlands, and Lithuania are pushing Brussels for faster emergency tariffs and anti-circumvention powers to counter Chinese industrial overcapacity. Here's what's at stake.

Trump says a US-Iran nuclear deal is 'largely negotiated.' Iran calls it a 'Persian-style peace.' Both sides claim victory. Here's what's actually at stake.

Thoughts

Share your thoughts on this article

Sign in to join the conversation