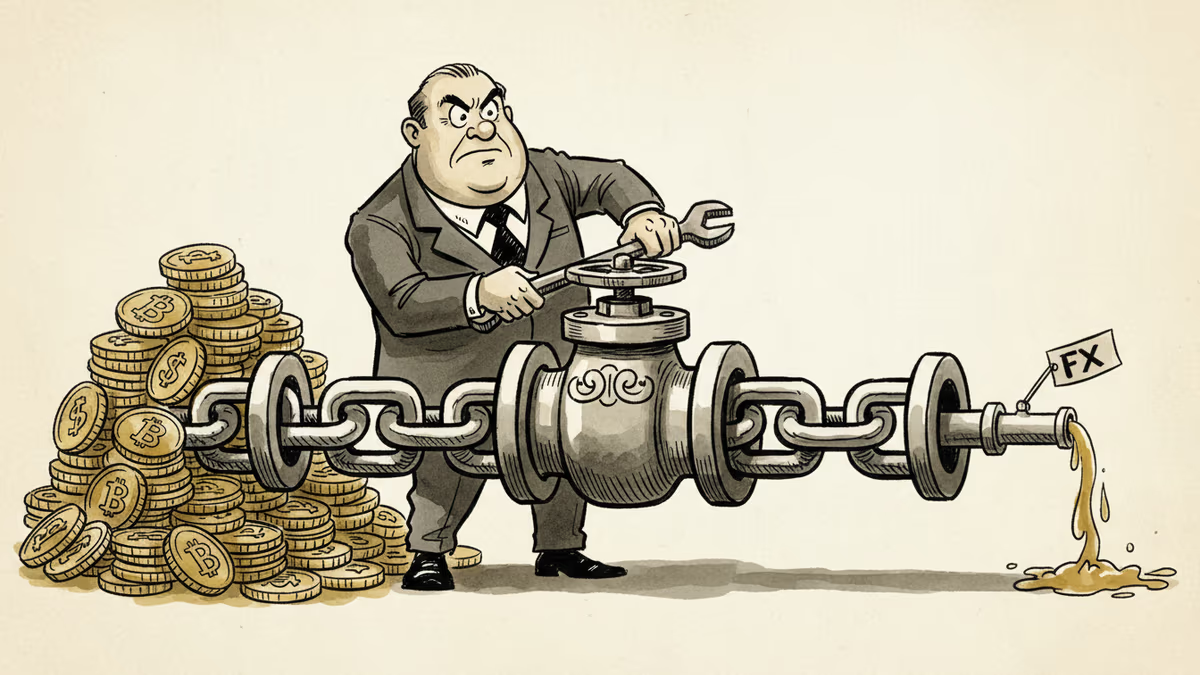

Brazil Just Banned Stablecoin Plumbing. The Rest of the World Is Watching.

Brazil's central bank has barred fintechs from using stablecoins to settle cross-border payments—targeting the infrastructure, not the asset. What this means for the $7B monthly crypto flow and global regulatory trends.

Brazil moves $6 to $8 billion in crypto every month. Stablecoins make up roughly 90% of that volume. On April 30, Brazil's central bank decided it had seen enough.

What the Rule Actually Does

BCB Resolution No. 561 doesn't ban crypto. That's the first thing to understand—and the detail most coverage is getting wrong. What it bans is a specific plumbing arrangement: electronic foreign exchange (eFX) providers using stablecoins or cryptocurrencies as the settlement layer for cross-border remittances. The rule takes effect October 1, with a compliance deadline stretching to May 2027 for firms seeking BCB authorization.

The practical target is a business model that's become surprisingly common. A remittance fintech takes reais from a Brazilian customer, converts them to USDT or USDC, and settles the payment abroad on a blockchain—bypassing traditional FX channels entirely. Nomad built exactly this, using Ripple's network to move money between Brazil and the U.S. and settling in stablecoins. Braza Bank went further, issuing its own real-backed stablecoin on the XRP Ledger.

Under Resolution 561, those back-end rails are closed. Cross-border settlements must now flow through a foreign exchange transaction or a non-resident real-denominated account held in Brazil. Individual investors, meanwhile, are untouched—buying, selling, and holding crypto remains legal under the separate framework established by Resolution BCB No. 521 in February.

Why This, Why Now

Brazil ranked fifth globally in crypto adoption in 2025, up from tenth the year before. Around 25 million Brazilians hold or transact in crypto. At that scale, stablecoins had quietly become a parallel FX channel—one that operated outside the central bank's visibility and control.

The timing adds context. In March, industry associations representing more than 850 companies pushed back against extending Brazil's IOF financial transaction tax to stablecoin operations. That fight isn't settled. Now, before the tax question is resolved, the BCB has moved to restrict the infrastructure itself. The sequencing suggests a deliberate strategy: don't just tax the flow, reshape the pipes.

Resolution 561 also expands eFX in one direction—providers can now handle transfers tied to financial and capital market investments, capped at $10,000 per transaction. The central bank isn't anti-fintech. It's drawing a perimeter.

Winners, Losers, and the Consumers Caught Between Them

The losers are the fintechs that built their competitive advantage on stablecoin efficiency. Lower fees and faster settlement times were the pitch. That pitch relied on blockchain's low transaction costs. Remove that layer, and the cost differential against traditional banks narrows—or disappears.

The winners are incumbent financial institutions: banks, securities brokers, and FX firms that already hold BCB authorization. They don't need to restructure anything. Smaller, unauthorized eFX operators face a harder choice: invest in compliance and apply for authorization by May 2027, or exit the market.

For consumers—particularly Brazil's diaspora communities and small importers—the most likely near-term effect is higher remittance costs. The efficiency that stablecoins delivered doesn't vanish; it gets absorbed somewhere in the chain. The question is who absorbs it.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

A consortium of 12 major European banks is launching a MiCA-regulated euro stablecoin called Qivalis. With 99.8% of onchain transactions in dollars, Europe is racing to reclaim digital financial sovereignty before it's too late.

Mastercard's $1.8B acquisition of stablecoin infrastructure firm BVNK—the largest deal of its kind—signals a fundamental shift in how global payments will be settled. Here's what it means for your money.

Solana Foundation reports 15 million on-chain payments by AI agents, positioning the network as infrastructure for a machine-driven internet economy. What happens when AI holds the wallet?

Mastercard's $1.8B acquisition of BVNK signals that stablecoins are no longer a crypto experiment — they're becoming the backbone of global payments. Here's what it means for your money, your industry, and the future of finance.

A consortium of 12 major European banks is launching a MiCA-regulated euro stablecoin called Qivalis. With 99.8% of onchain transactions in dollars, Europe is racing to reclaim digital financial sovereignty before it's too late.

Mastercard's $1.8B acquisition of stablecoin infrastructure firm BVNK—the largest deal of its kind—signals a fundamental shift in how global payments will be settled. Here's what it means for your money.

Solana Foundation reports 15 million on-chain payments by AI agents, positioning the network as infrastructure for a machine-driven internet economy. What happens when AI holds the wallet?

Mastercard's $1.8B acquisition of BVNK signals that stablecoins are no longer a crypto experiment — they're becoming the backbone of global payments. Here's what it means for your money, your industry, and the future of finance.

Thoughts

Share your thoughts on this article

Sign in to join the conversation