The Trillion-Dollar Autopilot: Who Really Pays When Index Funds Rebalance

Passive funds now control over $15 trillion in assets. Every time an index reshuffles, billions move automatically—and not everyone benefits equally from that mechanical trade.

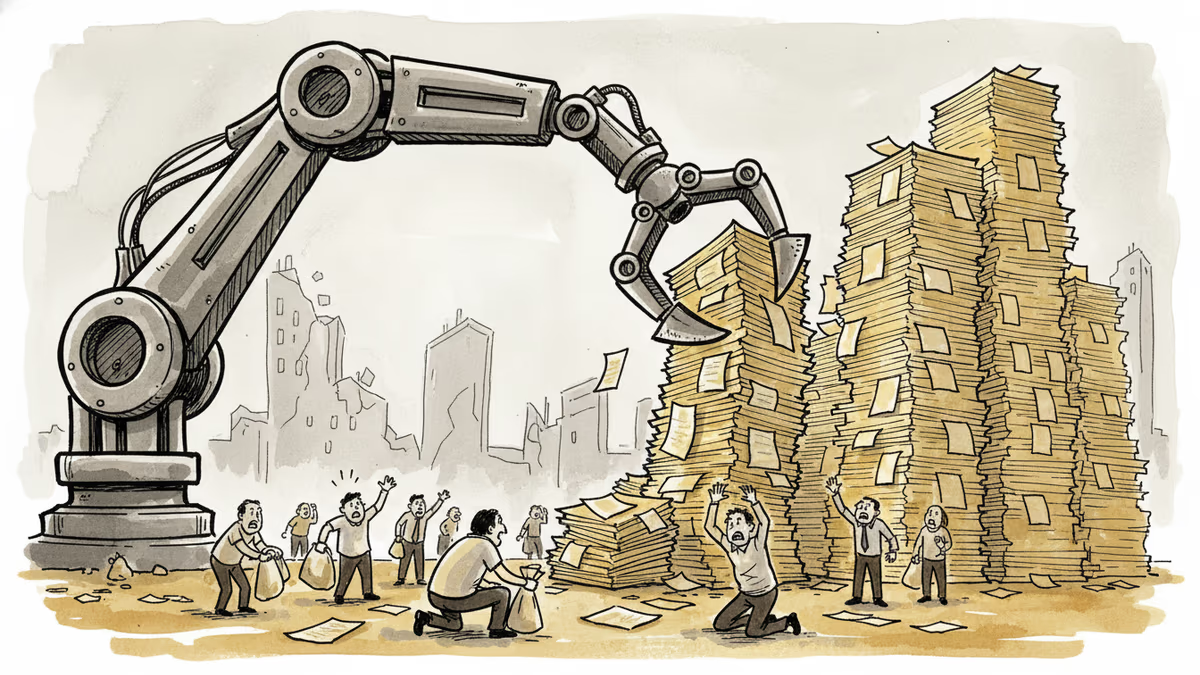

Every few months, billions of dollars change hands for one reason alone: a committee decided to update a list.

That's the quiet reality behind index rebalancing. When S&P Dow Jones Indices, MSCI, or FTSE Russell swap stocks in and out of their benchmarks, passive funds managing over $15 trillion in assets have no choice but to follow. No analysis. No debate. Buy what's in, sell what's out—on schedule, at scale.

With a fresh round of semi-annual rebalancing approaching, the mechanics of this system deserve a closer look. Because the money doesn't just move—it moves in ways that quietly disadvantage the very investors passive funds were designed to help.

How the Machine Works

Passive investing's pitch is elegant: instead of paying a fund manager to guess which stocks will win, just own the whole market. Keep costs low. Let compounding do the rest. The data broadly supports it—over the past 20 years, roughly 90% of active U.S. equity funds underperformed the S&P 500 after fees.

But passive funds don't actually own "the whole market." They own whatever the index says to own. And indexes change. When a company gets added to the S&P 500, every fund tracking that index must buy it—regardless of price. When a company gets cut, they must sell.

The announcement of these changes triggers what researchers call the Index Effect: an abnormal price move averaging 5–8% between the announcement date and the actual rebalancing date, as markets anticipate the forced trades to come. The stock going in rises. The stock going out falls. And passive funds, by design, execute on the wrong side of both moves.

The Arbitrage Hidden in Plain Sight

Hedge funds figured this out decades ago. The playbook is straightforward: buy the inclusion candidate the day it's announced, hold it while passive funds are obligated to accumulate, then sell into that demand on rebalancing day. Reverse the trade for deletions.

This strategy—sometimes called index arbitrage—isn't illegal. It's a rational response to a predictable, publicly announced, price-insensitive buyer. Academic estimates of the annual cost to passive investors from this dynamic range from the tens of billions to over $100 billion globally, though the figure is debated and difficult to isolate precisely.

The irony is structural. The more money flows into passive funds, the larger and more predictable the rebalancing trades become, and the more profitable the arbitrage. Passive investing's own success amplifies the inefficiency it creates.

Winners, Losers, and the Ordinary Investor

The winners in each rebalancing cycle are identifiable. Existing shareholders of newly added companies enjoy a price bump funded by mandatory buying. Hedge funds and quantitative traders who front-run the trades pocket the spread. Prime brokers facilitating the volume collect their fees.

The losers are less visible but more numerous: the retirement savers, 401(k) participants, and retail investors whose index funds and ETFs execute at slightly worse prices, cycle after cycle. Each individual drag is small—a few basis points here, a fraction of a percent there. Across $15 trillion in assets, the aggregate is not.

To be fair, the counterargument holds weight. Even accounting for this structural friction, most passive funds still outperform the average actively managed alternative after fees. The question isn't whether passive investing is bad—it's whether it's as cost-free as its marketing suggests.

A Market That Stops Asking "Why?"

Beyond the dollars, there's a broader concern that's harder to quantify. Markets function well when participants actively assess value—when buyers and sellers disagree about what a stock is worth and trade on that disagreement. That process, called price discovery, is how markets allocate capital to productive uses.

Passive funds don't participate in price discovery. They don't have a view on whether a stock is cheap or expensive. When passive strategies account for more than half of U.S. equity fund assets—as they now do—a growing share of daily trading is driven not by analysis but by index membership.

Some economists and former Federal Reserve officials have raised concerns that this shift could gradually impair market efficiency, making prices more sensitive to index inclusion than to underlying business performance. The counterargument is that active managers still set prices at the margin, and that passive investing's growth hasn't visibly broken anything yet.

Both positions have merit. The honest answer is that no one has run this experiment at this scale before.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

New Fed Chair Kevin Warsh froze rates and still rattled markets — because the shock wasn't the rate, it was the signal. Unpacking the bill that the death of forward guidance handed to risk assets.

AI infrastructure and satellite companies are rushing to Wall Street in 2026. What's driving the IPO wave, and what should investors watch for?

Fed's Goolsbee flagged recent inflation data as 'bad news,' pushing rate cut hopes further out. What that means for mortgages, markets, and your portfolio.

Tim Cook hands Apple's reins to John Ternus in September. Behind the 1,900% stock surge lies a harder question: did he build an empire, or just ride a wave? What investors need to know now.

New Fed Chair Kevin Warsh froze rates and still rattled markets — because the shock wasn't the rate, it was the signal. Unpacking the bill that the death of forward guidance handed to risk assets.

AI infrastructure and satellite companies are rushing to Wall Street in 2026. What's driving the IPO wave, and what should investors watch for?

Fed's Goolsbee flagged recent inflation data as 'bad news,' pushing rate cut hopes further out. What that means for mortgages, markets, and your portfolio.

Tim Cook hands Apple's reins to John Ternus in September. Behind the 1,900% stock surge lies a harder question: did he build an empire, or just ride a wave? What investors need to know now.

Thoughts

Share your thoughts on this article

Sign in to join the conversation