Why US LNG Can't Fill Qatar's Shoes When Push Comes to Shove

Analysis of structural limitations preventing US LNG producers from immediately replacing Qatari supply disruptions and global energy market implications

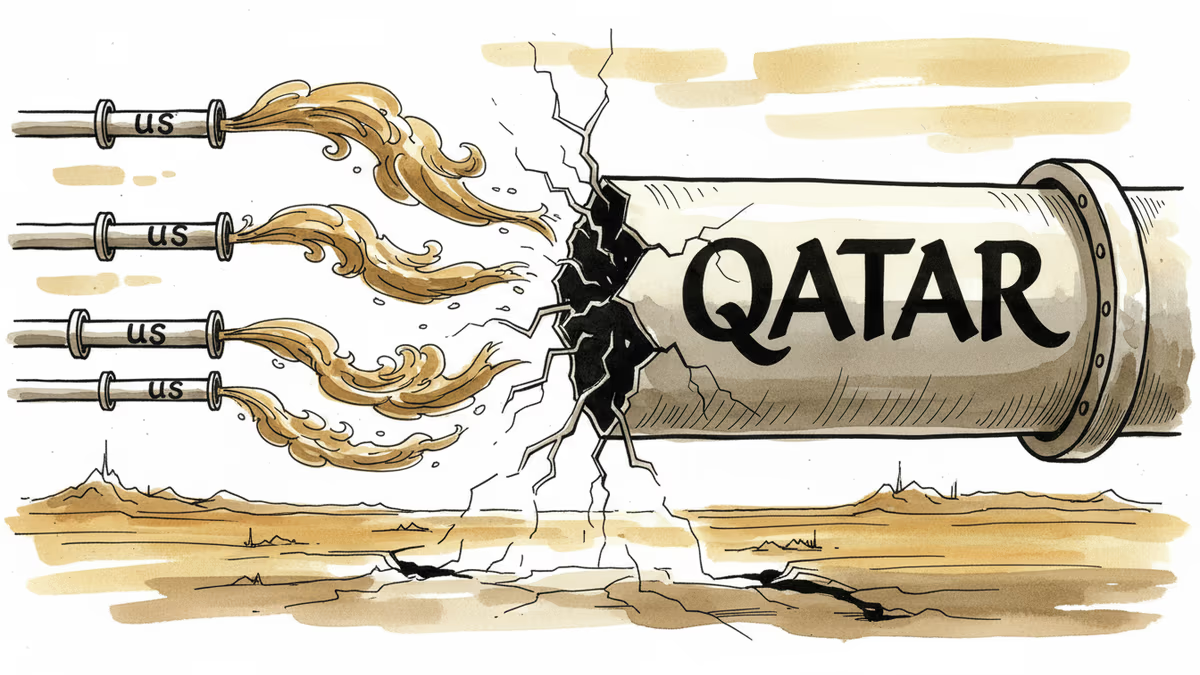

77 million tons per year. That's how much LNG Qatar ships to the world. If that tap suddenly turned off, could American producers step in? The uncomfortable truth: not a chance.

The Math Doesn't Add Up

Qatar controls 22% of global LNG trade. Even with America's shale gas boom, conjuring up 77 million tons of additional supply overnight isn't just difficult—it's physically impossible.

The bottleneck isn't just production capacity. LNG requires cooling natural gas to minus 162°F and specialized facilities that take 5-7 years to build. American companies could break ground tomorrow, but consumers wouldn't see that gas until the 2030s.

Cheniere Energy and Freeport LNG are already running their plants at full throttle. There's simply no spare capacity sitting idle, waiting for a Qatar crisis.

Winners, Losers, and Price Shocks

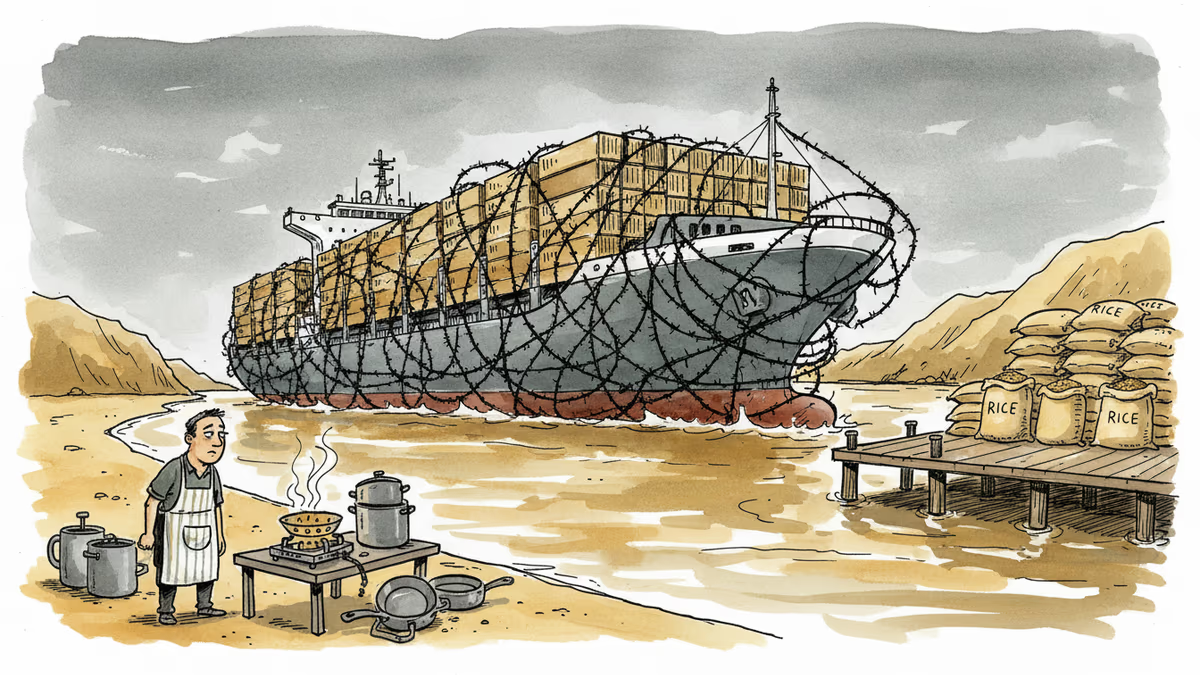

A Qatar supply disruption would create clear winners and losers. Asian buyers—Japan, South Korea, China—would face the biggest pain. They're Qatar's largest customers and would scramble for alternatives at premium prices.

American LNG producers, ironically, would hit the jackpot. Existing contracts would become gold mines as spot prices potentially triple. But this windfall comes with a catch: it would strain relationships with allies who'd face energy poverty.

European buyers might fare slightly better, having diversified after Russia's invasion of Ukraine. But "better" is relative when global LNG prices spike 200-300%.

The Infrastructure Reality Check

Here's what many miss: LNG isn't just about drilling more wells. The entire supply chain—liquefaction plants, specialized tankers, regasification terminals—operates as an integrated system.

America has 12 operational LNG export terminals with combined capacity of about 100 million tons annually. Qatar operates just 4 major facilities but they're massive, efficient, and strategically located for Asian markets.

Building new American capacity means navigating environmental reviews, securing financing for $10+ billion projects, and competing for skilled workers. The timeline stretches far beyond any short-term supply crisis.

Geopolitical Chess Game

Qatar's LNG leverage extends beyond market share. The country hosts America's largest Middle East military base while maintaining ties with Iran and Russia. This balancing act makes Qatar nearly sanction-proof—a calculated strategy that's paying dividends.

Meanwhile, American policymakers face their own dilemma. Pushing LNG exports too aggressively risks domestic price spikes and political backlash. The Biden administration already paused new export permits, citing climate concerns and domestic costs.

The Asian Dependency Problem

Asia's Qatar dependence runs deeper than numbers suggest. Long-term contracts, often 20+ years, create institutional relationships that can't be easily replaced. Japanese utilities like JERA and Korean KOGAS have built their entire procurement strategies around Qatari reliability.

These buyers would face a brutal choice: pay whatever the market demands or implement energy rationing. Neither option is politically palatable for governments already struggling with inflation.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

China's consumer prices hit a three-year low in April 2026. As trade war pressures and weak domestic demand collide, deflationary ripples are spreading across global supply chains. Here's what it means for your investments and industries.

Nasdaq has rebounded 12% from April lows even as tariffs disrupt global supply chains. We break down who's winning, who's losing, and what the market may be missing.

Energy analysts are stress-testing an 'Armageddon scenario' for gas markets — a strike on Qatar's LNG infrastructure. Here's what it means for prices, supply chains, and your wallet.

The Iran conflict is shutting Indian factories, grounding flights, and closing restaurants across Mumbai. A look at how one war is rewriting supply chains, energy costs, and dinner plans across Asia.

China's consumer prices hit a three-year low in April 2026. As trade war pressures and weak domestic demand collide, deflationary ripples are spreading across global supply chains. Here's what it means for your investments and industries.

Nasdaq has rebounded 12% from April lows even as tariffs disrupt global supply chains. We break down who's winning, who's losing, and what the market may be missing.

Energy analysts are stress-testing an 'Armageddon scenario' for gas markets — a strike on Qatar's LNG infrastructure. Here's what it means for prices, supply chains, and your wallet.

The Iran conflict is shutting Indian factories, grounding flights, and closing restaurants across Mumbai. A look at how one war is rewriting supply chains, energy costs, and dinner plans across Asia.

Thoughts

Share your thoughts on this article

Sign in to join the conversation