Kevin Warsh's Fed Nomination Signals Fundamental Rethink of Central Banking

Trump's nomination of Kevin Warsh as Fed Chair could reshape the central bank's role, moving away from expanded mandates toward traditional monetary policy focus.

The Federal Reserve may be about to undergo its most significant philosophical transformation in decades. Donald Trump's nomination of Kevin Warsh as Fed Chair isn't just another personnel change—it's a signal that the central bank's expanded role since the 2008 financial crisis is up for fundamental review.

A Goldman Sachs Veteran's Vision

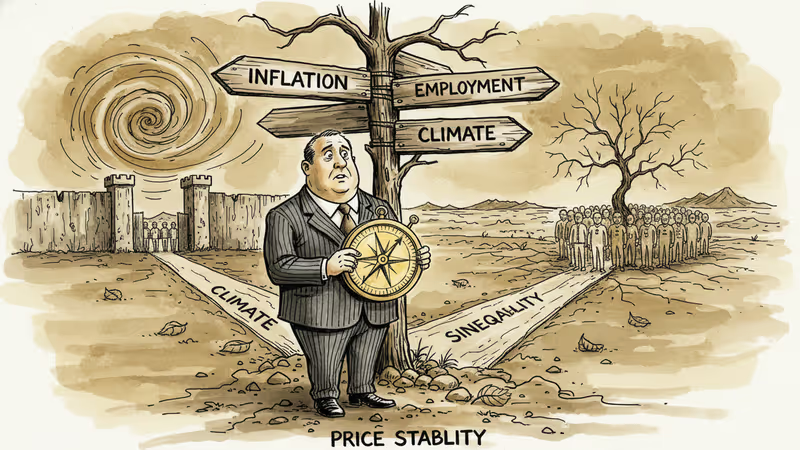

Warsh, who served as a Fed governor from 2006 to 2011 after his tenure at Goldman Sachs, has been a consistent critic of what economists call "mission creep"—the gradual expansion of central bank responsibilities beyond their core mandate. While current Fed policy encompasses everything from climate risk to social inequality, Warsh advocates for a return to basics: price stability and, to a lesser extent, employment.

His nomination comes at a time when the Fed's balance sheet remains near historic highs at over $7 trillion, and the central bank continues to play an outsized role in financial markets. Warsh has argued that this expansion has made the Fed "too big to succeed" and created dangerous dependencies in the financial system.

Market reactions have been swift. The dollar strengthened following news of his nomination, while long-term Treasury yields have risen as investors anticipate a more hawkish monetary stance. Bond traders are already pricing in a Fed that might be less accommodative and more focused on fighting inflation.

Global Central Banking at a Crossroads

The implications extend far beyond U.S. borders. Central banks worldwide have grappled with similar questions about their proper role since the financial crisis. The European Central Bank has ventured into climate policy, while the Bank of Japan continues unprecedented monetary accommodation. Warsh's potential leadership could force a global reckoning about what central banks should—and shouldn't—do.

For emerging markets, this shift could be particularly significant. A Fed focused primarily on price stability might pursue more predictable policies, reducing the boom-bust cycles that often plague developing economies when U.S. monetary policy shifts unexpectedly.

However, the transition period could bring volatility. If Warsh moves quickly to unwind some of the Fed's expanded programs, markets accustomed to central bank intervention might face adjustment challenges.

Three Pillars of Change

Warsh's approach would likely rest on three key principles. First, simplified objectives—prioritizing price stability over the current dual mandate that equally weights employment. Second, enhanced predictability—clearer communication about policy direction to reduce market uncertainty. Third, regulatory restraint—rolling back some post-crisis banking regulations that he views as unnecessarily restrictive.

Yet significant obstacles remain. Congressional confirmation won't be automatic, with Democrats likely to challenge his Wall Street background and deregulatory philosophy. Within the Fed itself, regional bank presidents and board members may resist dramatic policy shifts, creating potential internal tensions.

The international dimension adds complexity. If the U.S. pursues a more restrictive monetary policy while other major central banks maintain accommodation, currency volatility could spike, potentially disrupting global trade and investment flows.

Market Implications and Unintended Consequences

Financial markets are already adjusting expectations. Bank stocks have rallied on prospects of regulatory relief, while technology companies—sensitive to interest rate changes—have seen more muted reactions. Real estate markets, heavily dependent on Fed policy, face particular uncertainty.

But perhaps the most significant question involves unintended consequences. The Fed's expanded role didn't emerge in a vacuum—it developed in response to repeated financial crises and economic challenges that traditional monetary policy couldn't address alone. Simply returning to a narrower mandate might leave gaps that other institutions aren't equipped to fill.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Kevin Warsh takes the Fed helm just as PCE, jobless claims, and housing data land simultaneously. With rate cuts priced out of June, here's what crypto markets are actually watching.

Nvidia posted 85% revenue growth and a $80B buyback. Its stock still dropped — for the fourth straight post-earnings quarter. Here's what that tells us about where AI investing stands right now.

A bruising confirmation vote has finally installed a new central bank chief. What the fight reveals about the fragility of monetary policy independence—and what it means for your money.

Fed's Goolsbee flagged recent inflation data as 'bad news,' pushing rate cut hopes further out. What that means for mortgages, markets, and your portfolio.

Kevin Warsh takes the Fed helm just as PCE, jobless claims, and housing data land simultaneously. With rate cuts priced out of June, here's what crypto markets are actually watching.

Nvidia posted 85% revenue growth and a $80B buyback. Its stock still dropped — for the fourth straight post-earnings quarter. Here's what that tells us about where AI investing stands right now.

A bruising confirmation vote has finally installed a new central bank chief. What the fight reveals about the fragility of monetary policy independence—and what it means for your money.

Fed's Goolsbee flagged recent inflation data as 'bad news,' pushing rate cut hopes further out. What that means for mortgages, markets, and your portfolio.

Thoughts

Share your thoughts on this article

Sign in to join the conversation