Your Pension Fund Wants Bitcoin. Should You Worry?

Indiana joins 21 US states investing public funds in bitcoin while simultaneously banning crypto ATMs due to fraud. The contradiction reveals America's complex relationship with digital assets.

$400,000. That's how much residents of Evansville, Indiana lost to crypto ATM scams in 2025. Yet the same state just passed a law allowing public employee pensions to invest in bitcoin. Welcome to America's schizophrenic relationship with cryptocurrency.

The Great State Bitcoin Rush

Indiana's HB 1042 authorizes public retirement and savings plans to buy digital assets and spot crypto ETFs. Governor Mike Braun is expected to sign it within 10 days, making Indiana the latest state to embrace what was once considered financial heresy.

The numbers tell the story: 21 states are now investing in or evaluating bitcoin for public funds. Wyoming led the charge, followed by Wisconsin, Michigan, and Arizona. Tennessee, Oklahoma, and Nebraska have joined the club.

This isn't happening in a vacuum. President Trump's push for a "Bitcoin Strategic Reserve" has unleashed a state-level arms race. The message is clear: get on board or get left behind.

The Fraud Paradox

Here's where it gets interesting. On the same day Indiana embraced bitcoin for pensions, lawmakers banned crypto ATMs statewide. The reason? Those $400,000 in Evansville scams weren't isolated incidents.

The FBI reports Americans lost $240 million to crypto ATM fraud in the first half of 2025 alone. Complaints surged 99% from 2023 to 2024, reaching nearly 11,000 cases.

The message seems to be: crypto is fine for institutions, dangerous for individuals. Massachusetts Attorney General sued Bitcoin Depot, alleging its machines enabled criminal scams. Yet pension fund managers are being told bitcoin belongs in retirement portfolios.

Your Money, Their Rules

For public employees, this creates an uncomfortable reality. Your pension fund—the money securing your retirement—might soon include an asset so volatile that ATMs selling it are being banned as public hazards.

Consider the math: bitcoin has delivered 47% annual returns over five years. Traditional pension investments? Much lower, but also much more predictable. The question isn't whether bitcoin can make money—it's whether it belongs in funds designed to provide steady retirement income.

Pension fund managers face a different calculus than individual investors. They can't afford to lose retirees' money chasing returns. But they also can't afford to miss out on generational wealth creation while inflation erodes traditional assets.

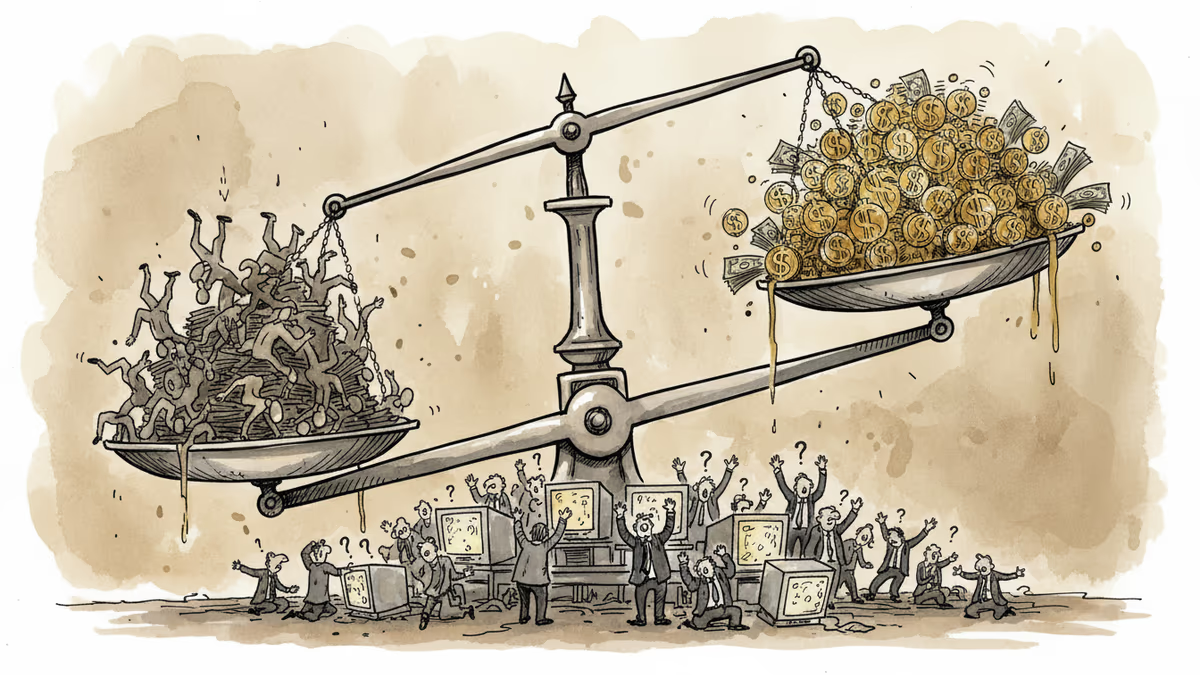

The Institutional Divide

What's emerging is a two-tier system: sophisticated institutions get access to bitcoin's upside, while retail investors are protected from its risks through ATM bans and stricter regulations.

This raises uncomfortable questions about financial equality. Should pension funds get bitcoin exposure that individual savers can't easily access? Or are regulators right to treat institutional and retail investors differently?

The trend suggests we're moving toward a world where your exposure to crypto depends more on who manages your money than your personal risk tolerance.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Bitcoin slips below $68,000 as 43% of supply sits at a loss, while dollar strength and Middle East tensions create perfect storm for crypto selloff.

Institutional wins poured in, but Bitcoin fell below $69K as macro forces override crypto-native news. The price of mainstream adoption may be losing independence.

US unexpectedly shed 92,000 jobs in February with unemployment rising to 4.4%, sparking Fed rate cut speculation despite inflation concerns from rising oil prices

Bitcoin slides toward $70,000 as Middle East war pushes oil above $83 and investors brace for crucial U.S. employment data. Risk-off sentiment grips markets.

Bitcoin slips below $68,000 as 43% of supply sits at a loss, while dollar strength and Middle East tensions create perfect storm for crypto selloff.

Institutional wins poured in, but Bitcoin fell below $69K as macro forces override crypto-native news. The price of mainstream adoption may be losing independence.

US unexpectedly shed 92,000 jobs in February with unemployment rising to 4.4%, sparking Fed rate cut speculation despite inflation concerns from rising oil prices

Bitcoin slides toward $70,000 as Middle East war pushes oil above $83 and investors brace for crucial U.S. employment data. Risk-off sentiment grips markets.

Thoughts

Share your thoughts on this article

Sign in to join the conversation