One Click, 2.5GB of Personal Data Gone

Figure Technology's social engineering breach exposes fintech vulnerabilities. How single sign-on systems create cascading security risks across the financial sector.

When Human Error Becomes Corporate Crisis

Figure Technology confirmed what every CISO fears most: one employee's mistake exposed thousands of customers' personal data. The blockchain-based lending giant admitted hackers stole 2.5GB of files after an employee fell for a social engineering attack. The stolen data included full names, home addresses, birth dates, and phone numbers.

The hacking group ShinyHunters claimed responsibility, publishing the data on their dark web site after Figure refused to pay ransom. But this wasn't an isolated attack—it was part of a broader campaign targeting companies that rely on Okta's single sign-on services. Harvard University and the University of Pennsylvania were also hit.

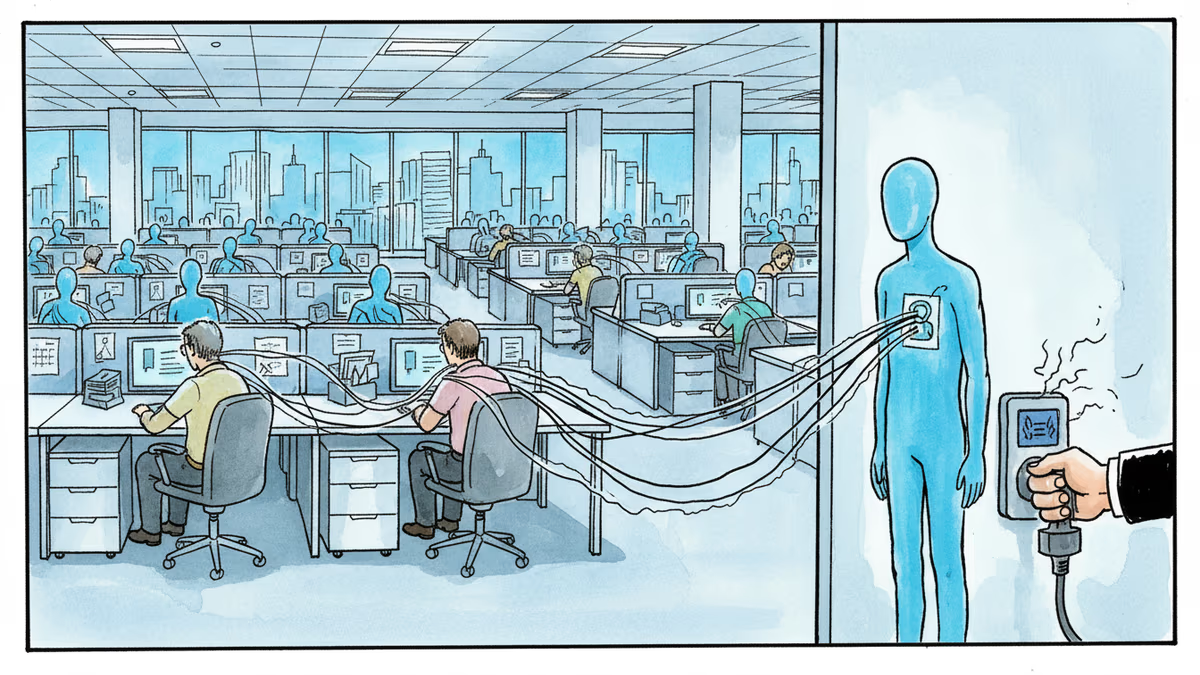

The SSO Domino Effect: Convenience Meets Catastrophe

Single sign-on systems are everywhere in fintech. They're convenient, cost-effective, and users love them. One password gets you into everything. But they also create a single point of failure that can cascade across entire organizations.

Think about your own digital life. How many financial services do you access through Google, Microsoft, or Apple logins? Each connection creates potential exposure. When Okta customers get breached, it's not just about one company—it's about the entire ecosystem of connected services.

For fintech companies, the math is brutal. Building proprietary authentication systems costs millions and slows product launches. Using third-party SSO providers saves money and accelerates time-to-market. But as Figure learned, that convenience comes with hidden costs.

The Industry's Security Paradox

Customers demand seamless experiences. They want to open bank accounts in minutes, get loans approved instantly, and invest with a few taps. Any friction drives them to competitors.

Investors push for rapid growth and user acquisition. Security investments don't show immediate returns, while user experience improvements drive obvious metrics. The pressure to prioritize features over security is intense.

Regulators face their own dilemma. Heavy-handed security requirements could stifle fintech innovation and push consumers back to traditional banks. But light regulation leaves consumers vulnerable to exactly these kinds of breaches.

Security professionals are caught in the middle, trying to balance risk management with business objectives. As one cybersecurity executive told me: "We're always playing defense while the business wants to move fast and break things. But in fintech, breaking things means breaking trust."

Authors

Related Articles

UK Visa Portal, a private immigration service mistaken for an official government site, has been exposing passport scans and selfies of over 100,000 applicants. The breach remains unpatched.

Okta CEO Todd McKinnon on why AI agents need identity management, the SaaSpocalypse threat, and why the kill switch might be the most important button in enterprise tech.

Despite fierce competition, the CEOs of Polymarket and Kalshi have co-invested in 5(c) Capital, a $35M VC fund targeting prediction market infrastructure. What this signals for the industry.

A class action lawsuit accuses Kalshi of changing payout rules after Iran's Supreme Leader Khamenei was killed. The case cuts to the heart of prediction market credibility.

UK Visa Portal, a private immigration service mistaken for an official government site, has been exposing passport scans and selfies of over 100,000 applicants. The breach remains unpatched.

Okta CEO Todd McKinnon on why AI agents need identity management, the SaaSpocalypse threat, and why the kill switch might be the most important button in enterprise tech.

Despite fierce competition, the CEOs of Polymarket and Kalshi have co-invested in 5(c) Capital, a $35M VC fund targeting prediction market infrastructure. What this signals for the industry.

A class action lawsuit accuses Kalshi of changing payout rules after Iran's Supreme Leader Khamenei was killed. The case cuts to the heart of prediction market credibility.

Thoughts

Share your thoughts on this article

Sign in to join the conversation