Bitcoin Miners Split Into Winners and Losers as Wall Street Picks Sides

Morgan Stanley's first bitcoin miner coverage reveals a stark divide - data center converters get buy ratings while pure miners face sell recommendations. A new paradigm for crypto infrastructure?

Wall Street just drew a line in the sand for bitcoin miners. On one side: companies pivoting to data centers. On the other: those still betting everything on bitcoin's wild ride. Morgan Stanley's verdict? Only one strategy deserves your money.

The Great Divide

Morgan Stanley initiated coverage of three bitcoin miners Monday with starkly different recommendations. Cipher Mining (CIFR) and TeraWulf (WULF) earned "Overweight" ratings with price targets of $38 and $37 respectively - more than double their current trading levels.

Marathon Digital (MARA) wasn't so lucky. It got slapped with an "Underweight" rating and an $8 target, barely above where it trades today.

The market's response was swift. CIFR surged 12.4% to $16.51, while WULF jumped 12.8% to $16.12. Marathon managed only modest gains, trading at $8.28.

Analyst Stephen Byrd's reasoning cuts to the heart of what bitcoin mining companies are becoming - or should become.

Infrastructure vs. Speculation

Byrd's core thesis treats certain mining operations less like crypto plays and more like infrastructure assets. Once a mining company builds a data center and signs long-term leases with creditworthy tenants, he argues, "that DC's natural investor habitat is not among bitcoin investors but among infrastructure investors."

The comparison is telling. Byrd points to data center REITs like Equinix (EQIX) and Digital Realty (DLR), which trade at over 20 times forward EBITDA. Investors willingly pay $20+ for every $1 of expected annual cash flow because these companies offer scale, diversification, and predictable growth.

Cipher Mining sits at the center of this "REIT endgame" vision. The company's data centers could theoretically operate like toll roads - charging predictable fees regardless of bitcoin's price swings. TeraWulf gets similar treatment, with Byrd highlighting management's power infrastructure background and track record of signing data center agreements.

Marathon tells a different story. The company doubled down on bitcoin exposure, issuing convertible notes to buy more bitcoin directly. "For MARA, bitcoin mining economics are the dominant driver of the stock's value," Byrd wrote - and that's precisely the problem.

The Mining Math Problem

Behind the ratings lies a harsh reality about bitcoin mining economics. "The historical ROIC of the bitcoin mining business has been unattractive," Morgan Stanley noted, pointing to "significant risks to profitability" both near and long-term.

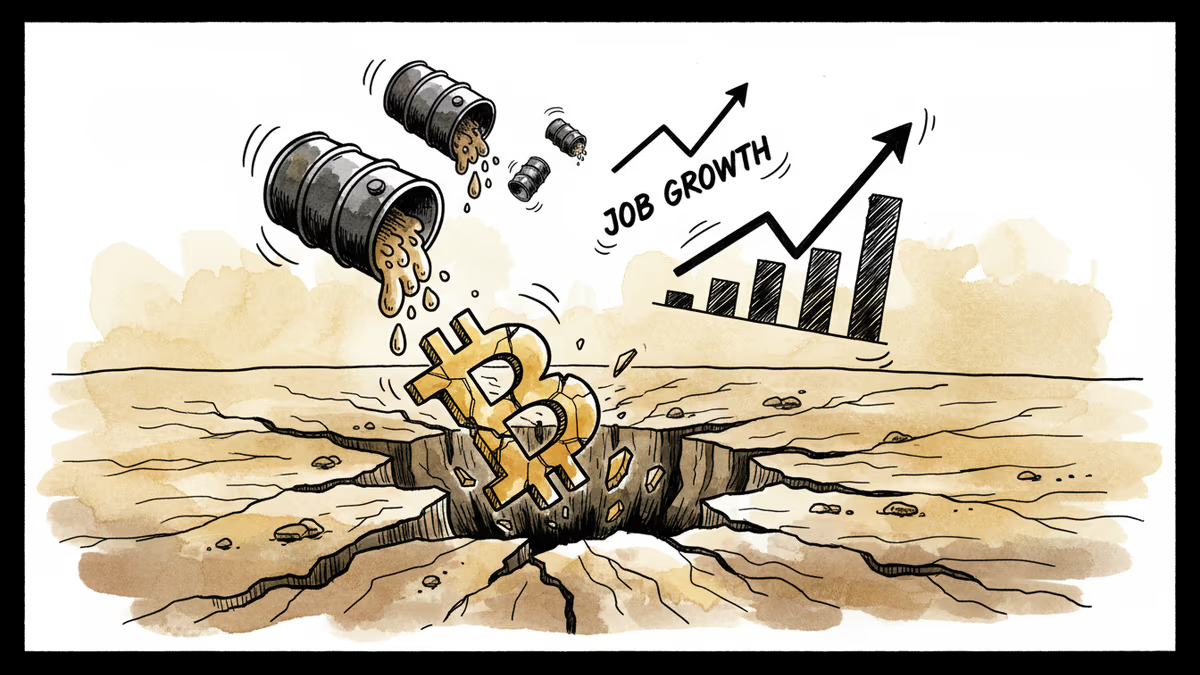

The numbers tell the story. Every four years, bitcoin's halving event cuts mining rewards in half. April 2024's halving left many miners struggling with the same electricity costs but half the revenue. Meanwhile, the AI boom created a more lucrative alternative - renting out those same facilities to companies training AI models.

NVIDIA GPUs generate far higher returns powering AI workloads than mining bitcoin. It's simple economics driving the industry's pivot.

The choice facing bitcoin miners mirrors a broader question for the entire crypto industry: mature into regulated infrastructure or remain in speculative territory?

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Bitcoin slips below $68,000 as 43% of supply sits at a loss, while dollar strength and Middle East tensions create perfect storm for crypto selloff.

Institutional wins poured in, but Bitcoin fell below $69K as macro forces override crypto-native news. The price of mainstream adoption may be losing independence.

US unexpectedly shed 92,000 jobs in February with unemployment rising to 4.4%, sparking Fed rate cut speculation despite inflation concerns from rising oil prices

Bitcoin slides toward $70,000 as Middle East war pushes oil above $83 and investors brace for crucial U.S. employment data. Risk-off sentiment grips markets.

Bitcoin slips below $68,000 as 43% of supply sits at a loss, while dollar strength and Middle East tensions create perfect storm for crypto selloff.

Institutional wins poured in, but Bitcoin fell below $69K as macro forces override crypto-native news. The price of mainstream adoption may be losing independence.

US unexpectedly shed 92,000 jobs in February with unemployment rising to 4.4%, sparking Fed rate cut speculation despite inflation concerns from rising oil prices

Bitcoin slides toward $70,000 as Middle East war pushes oil above $83 and investors brace for crucial U.S. employment data. Risk-off sentiment grips markets.

Thoughts

Share your thoughts on this article

Sign in to join the conversation