The Price Hike You Haven't Noticed Yet Is Already Built Into Your Next Car

Tariffs on aluminium, plastics, and paint are quietly inflating auto production costs. Here's who pays, who profits, and what it means for the EV transition.

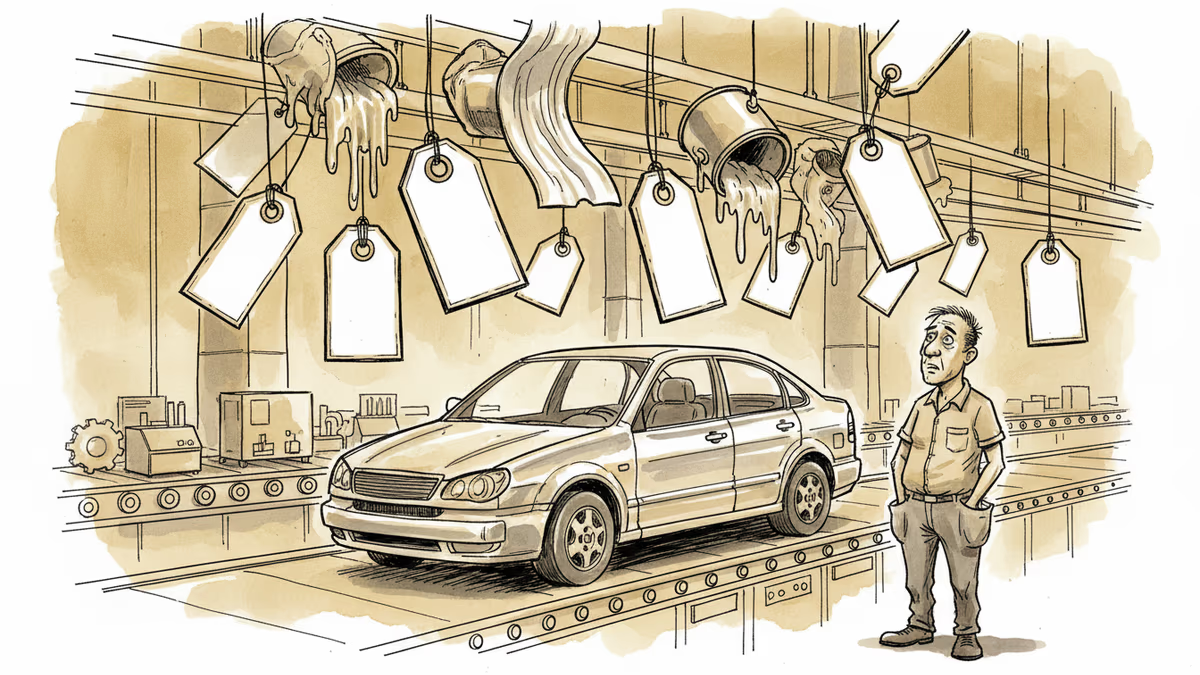

The sticker price on your next car hasn't moved yet. But the cost to build it already has.

The latest wave of tariff pressure isn't hitting finished vehicles at the port—it's hitting the raw materials that go into every bolt, panel, and coat of paint long before the car reaches a showroom. Aluminium, high-grade plastics, copper wiring, and automotive paint are all facing simultaneous cost increases, and the auto industry is quietly absorbing a bill it will eventually pass on.

What's Actually Getting More Expensive

A modern passenger vehicle contains roughly 2,000 individual parts sourced from hundreds of suppliers across multiple countries. The materials underpinning those parts—aluminium for body panels and engine components, engineering plastics for bumpers and interiors, copper for wiring harnesses, and speciality coatings for exterior finishes—are all caught in the same tariff crossfire.

The US 25% tariff on steel and aluminium, combined with broader levies on goods from key supplier countries, has pushed raw material procurement costs up across the board. Industry estimates suggest the added materials cost per mid-size vehicle now runs into the hundreds of dollars, depending on the model's material mix and where its supply chain sits.

That number sounds manageable in isolation. Spread it across millions of vehicles, and it becomes a margin crisis for the companies that can't immediately renegotiate contracts or shift sourcing.

Winners, Losers, and the People Stuck in the Middle

The impact isn't uniform. Where you sit in the supply chain determines whether this is a problem or an opportunity.

Tier-2 and Tier-3 suppliers are absorbing the most pain. Long-term contracts with fixed unit prices mean they can't pass cost increases upstream quickly. Many are already in renegotiation talks with OEMs, but those conversations take time—and margins erode in the interim. Some smaller suppliers are quietly reviewing headcount.

Materials producers, by contrast, are seeing pricing power they haven't had in years. Aluminium smelters and speciality chemical companies supplying automotive-grade plastics and coatings are converting price increases into revenue—at least for now. If demand softens as vehicle prices rise, that tailwind reverses.

For consumers, the math is straightforward. Ford, GM, Stellantis, Toyota, Hyundai-Kia—every major OEM faces the same upstream pressure. The question isn't whether prices rise; it's who blinks first and by how much. When new car prices climb, buyers migrate to used vehicles. US used-car prices are already showing early signs of renewed upward pressure, according to dealer-level data—a pattern that echoes the post-pandemic supply shock of 2021-2022.

Electric Vehicles Are More Exposed Than You'd Think

Here's the counterintuitive wrinkle: EVs, widely seen as the industry's future, are disproportionately vulnerable to this specific cost shock.

Electric vehicles use 20–30% more aluminium than comparable internal combustion vehicles, driven by the need to offset battery weight with lighter structural components. Their large, integrated body structures also require more complex—and more expensive—paint processes. Add the materials cost already embedded in battery packs, and EV manufacturers are facing a compounding squeeze at precisely the moment they're trying to compete on price with legacy combustion vehicles.

Tesla has been cutting prices aggressively to defend market share. Rivian is still working toward consistent profitability. Startups across the EV space had built cost-reduction roadmaps that assumed stable or falling input prices. Those roadmaps need rewriting.

The Policy Intention vs. The Actual Effect

The stated logic behind materials tariffs is domestic industrial revival—bring production home, rebuild manufacturing capacity, reduce dependence on foreign supply chains. There's a reasonable long-term argument for that.

The short-term reality is messier. Domestic aluminium and steel capacity can't scale overnight to replace import volumes. In the interim, manufacturers pay more, consumers pay more, and the transition to EVs—which requires more of the materials being taxed—gets more expensive, not less.

This gap between policy intention and market effect isn't unique to the auto sector, but it's particularly visible here because the numbers are large and the supply chains are global by design. A car built in Michigan still contains aluminium rolled in Canada, plastics compounded in Germany, and rare earth elements processed in China.

This content is AI-generated based on source articles. While we strive for accuracy, errors may occur. We recommend verifying with the original source.

Related Articles

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Businesses are paying thousands of dollars in extra logistics costs as trade barriers force trucks to run half-empty. Here's who pays, who profits, and what it means for prices.

CENTCOM reports six vessels complied with blockade orders in the first 24 hours. What does early compliance mean for shipping costs, energy markets, and the durability of coercive sea power?

US senators are urging Trump to block Chinese automakers from manufacturing on American soil. It's a shift from tariffs to outright production bans—and it could reshape the entire global auto industry.

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Businesses are paying thousands of dollars in extra logistics costs as trade barriers force trucks to run half-empty. Here's who pays, who profits, and what it means for prices.

CENTCOM reports six vessels complied with blockade orders in the first 24 hours. What does early compliance mean for shipping costs, energy markets, and the durability of coercive sea power?

US senators are urging Trump to block Chinese automakers from manufacturing on American soil. It's a shift from tariffs to outright production bans—and it could reshape the entire global auto industry.

Thoughts

Share your thoughts on this article

Sign in to join the conversation