Why Japan's Biggest Banks Are Buying Bonds Despite Mounting Losses

Japan's megabanks are preparing to increase JGB holdings despite growing losses from their bond portfolios. An analysis of banking strategy in a low-rate environment.

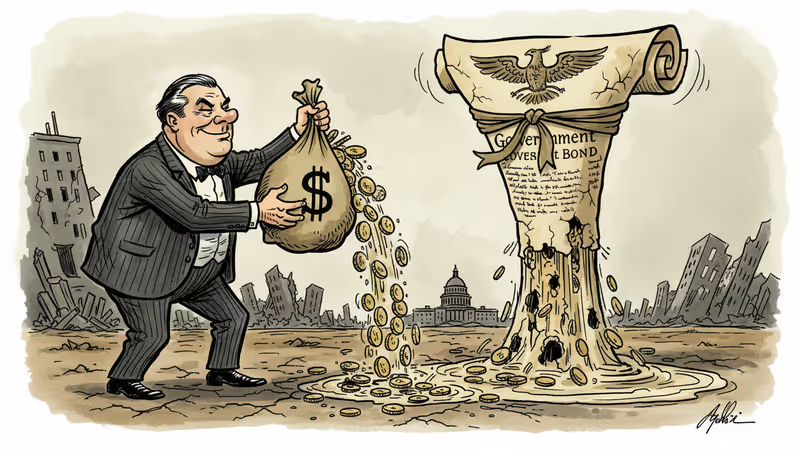

Japan's three largest banks are doubling down on a losing bet. Despite mounting losses from their government bond portfolios, Mitsubishi UFJ, Mizuho, and Sumitomo Mitsui are preparing to increase their holdings of Japanese Government Bonds (JGBs).

The Paradox of Safe Investments

At first glance, this strategy seems counterintuitive. 10-year JGB yields hover around 1%, barely covering operational costs. Meanwhile, the Bank of Japan's gradual shift toward policy normalization has triggered mark-to-market losses on existing bond holdings across the banking sector.

Yet these institutions see no alternative. Corporate loan demand remains sluggish, overseas investments carry significant currency risks, and regulatory capital requirements favor government securities. The banks are essentially trapped in a cycle where the safest assets offer the poorest returns.

Mitsubishi UFJ alone holds over ¥50 trillion in deposits but struggles to deploy this capital profitably. With loan-to-deposit ratios well below 70% across major Japanese banks, excess liquidity has become both a blessing and a curse.

A Glimpse into Banking's Future

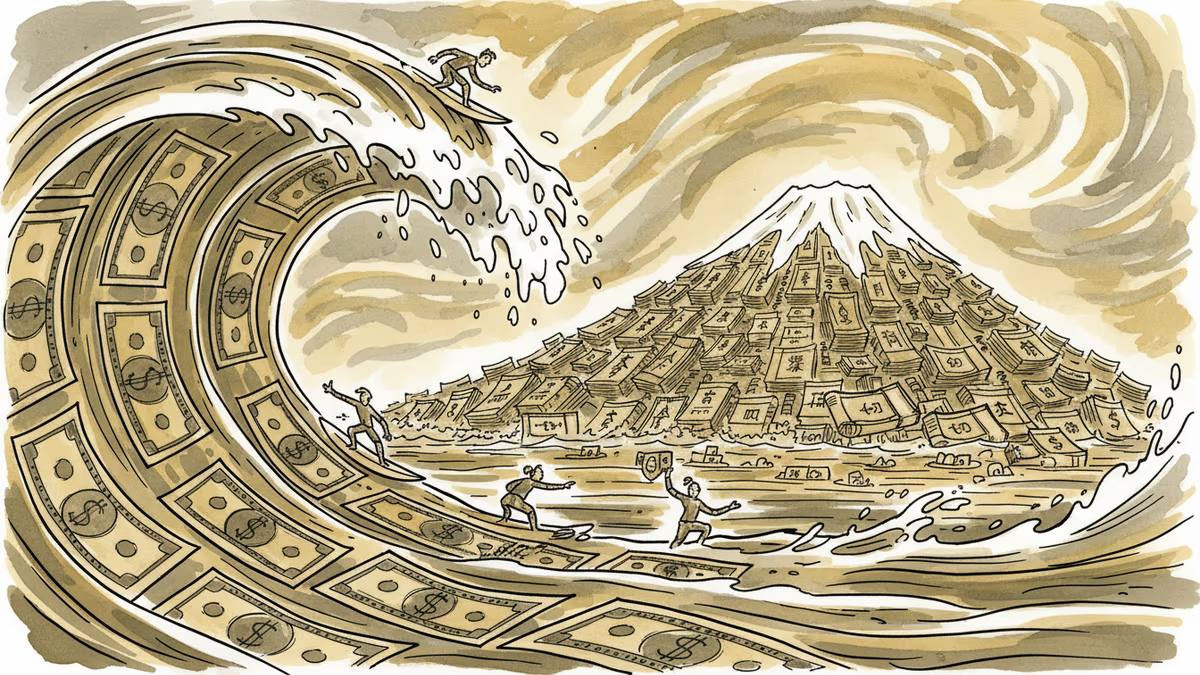

This Japanese scenario offers a preview of challenges facing banks globally as interest rates remain structurally low. The traditional banking model—borrowing short and lending long—breaks down when yield curves flatten and credit demand stagnates.

European banks face similar pressures, with the European Central Bank's negative interest rate policies creating comparable dilemmas. Even U.S. regional banks, despite higher rates, grapple with commercial real estate exposures and deposit flight to money market funds.

The Japanese experience suggests that banks may need to fundamentally reimagine their business models. Some are exploring fee-based services, wealth management, and fintech partnerships, but these revenue streams can't fully replace traditional lending margins.

The Regulatory Angle

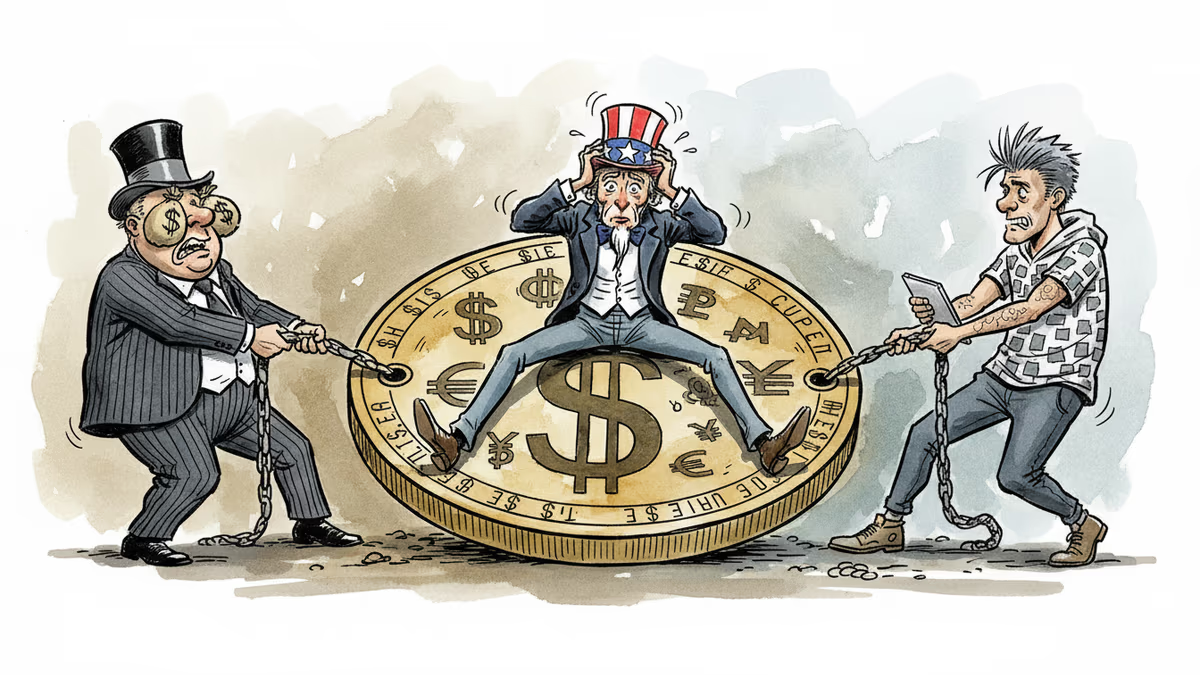

Regulators face their own paradox here. Basel III requirements encourage banks to hold government securities, yet these same assets are becoming liability drains. Japanese financial authorities must balance systemic stability against individual bank profitability.

This tension extends beyond Japan. As central banks worldwide consider rate cuts to combat economic slowdowns, they risk creating similar scenarios where banks become reluctant holders of low-yielding sovereign debt.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Crypto-friendly fintech giant Revolut files for U.S. banking license, potentially disrupting traditional banking with direct Fed access and lending capabilities. Following Kraken's master account approval, the fintech revolution accelerates.

Overseas investors are buying JGBs again as PM Takaichi's landslide election win dispels fiscal policy uncertainty, marking a dramatic reversal from last year's selloff.

Trump's crypto adviser rejects JPMorgan CEO's call for bank-like regulation of yield-bearing stablecoins, highlighting growing tensions between traditional finance and crypto innovation

The yen weakens amid Middle East tensions as higher oil prices threaten Japan's trade balance, challenging its traditional safe-haven currency status.

Crypto-friendly fintech giant Revolut files for U.S. banking license, potentially disrupting traditional banking with direct Fed access and lending capabilities. Following Kraken's master account approval, the fintech revolution accelerates.

Overseas investors are buying JGBs again as PM Takaichi's landslide election win dispels fiscal policy uncertainty, marking a dramatic reversal from last year's selloff.

Trump's crypto adviser rejects JPMorgan CEO's call for bank-like regulation of yield-bearing stablecoins, highlighting growing tensions between traditional finance and crypto innovation

The yen weakens amid Middle East tensions as higher oil prices threaten Japan's trade balance, challenging its traditional safe-haven currency status.

Thoughts

Share your thoughts on this article

Sign in to join the conversation