Vestas Picks Japan. What Does That Say About Asia's Wind Race?

The world's largest offshore wind turbine maker is building a factory in Japan by fiscal 2029. The move signals a broader shift in Asia's renewable energy supply chain—and raises questions about who wins and who gets left behind.

When the world's biggest wind turbine maker decides where to plant its next factory, it's not just a logistics call—it's a verdict on which country is serious about the energy transition.

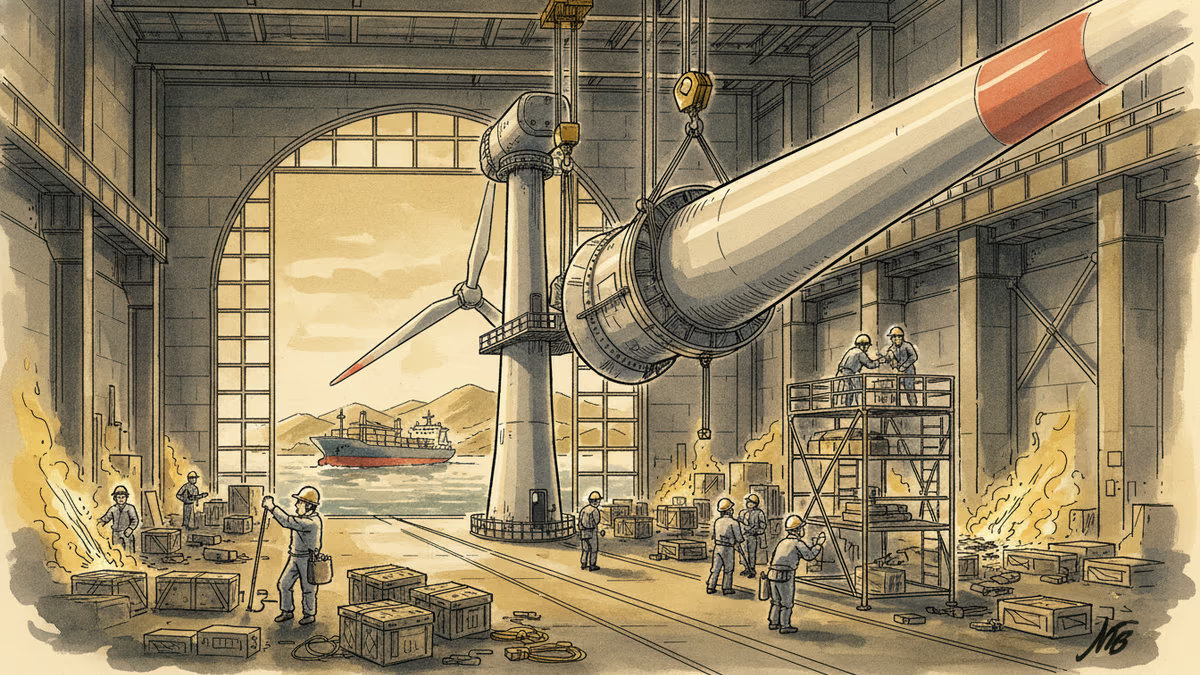

Vestas, the Danish company that dominates the global offshore wind turbine market, is building a manufacturing facility in Japan, targeting completion by fiscal year 2029, Nikkei reported. The plant is designed to serve Japan's surging domestic demand and act as a supply hub for the broader Asia-Pacific region.

The Math Behind the Move

The business case is straightforward. Offshore wind turbines are enormous—blades alone can stretch over 100 meters. Shipping them from European factories to Asian project sites burns a significant share of project economics. Local manufacturing doesn't just cut costs; in a competitive tender environment, it can be the difference between winning and losing a contract.

Japan has given Vestas plenty of reason to commit. The government has set targets of 10 GW of offshore wind capacity by 2030 and 30–45 GW by 2040. TEPCO, Japan's largest utility, recently announced plans to spend $70 billion over the next decade on grid upgrades to accommodate that capacity. That's not a market—that's a pipeline.

Timing matters too. With the U.S. IRA facing political headwinds and European demand growth slowing, Asia has become the most consequential battleground for the next decade of renewable energy deployment. Vestas is positioning itself ahead of competitors like Siemens Gamesa and China's CSSC, both of whom are also eyeing the region.

Japan's Regulatory Tailwind

Capacity targets alone don't attract factories. Japan has been quietly dismantling the bureaucratic friction that historically slowed renewable energy projects. Permitting reforms have compressed timelines, and the government has moved to designate specific offshore zones for development—reducing the uncertainty that deters long-term capital commitments.

That regulatory clarity is itself a competitive asset. Vestas isn't just betting on Japanese demand; it's betting that Japan will be able to build at the pace its targets require. That confidence, embedded in a multi-year factory investment, is a meaningful signal.

Winners, Losers, and the Broader Stakes

For Japanese developers and utilities, the benefits are tangible: shorter lead times, lower component costs, and reduced exposure to global shipping disruptions—something the industry felt acutely during the post-pandemic supply chain crunch.

For Vestas, the plant strengthens its position across Southeast Asia, where Vietnam, the Philippines, and Taiwan are all accelerating offshore wind development. A Japan-based factory can serve that entire arc more efficiently than any European facility.

For investors in renewables, the move reinforces a broader trend: supply chain localization is becoming a core competitive strategy, not just a risk-management footnote. Companies that control regional manufacturing will have structural cost advantages as Asian markets scale.

The more complicated picture is for South Korea. Seoul has its own offshore wind ambitions—14.3 GW by 2030—and domestic players like Doosan Enerbility and CS Wind have been building turbine and component capabilities. CS Wind, notably, is already a key Vestas supplier, which means this factory decision could represent opportunity as much as competition. But the fact that Vestas chose Japan over Korea as its regional anchor raises a pointed question about permitting timelines, community acceptance processes, and the overall ease of doing business in Korea's offshore wind sector.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Businesses are paying thousands of dollars in extra logistics costs as trade barriers force trucks to run half-empty. Here's who pays, who profits, and what it means for prices.

Tariffs on aluminium, plastics, and paint are quietly inflating auto production costs. Here's who pays, who profits, and what it means for the EV transition.

Nations obsessed with military deterrence have discovered a more powerful lever—critical minerals. How the race for rare earths is reshaping geopolitics, supply chains, and global security.

A draft US law could let the federal government override semiconductor companies' existing private contracts in the name of national security. Here's what's at stake for the industry.

Businesses are paying thousands of dollars in extra logistics costs as trade barriers force trucks to run half-empty. Here's who pays, who profits, and what it means for prices.

Tariffs on aluminium, plastics, and paint are quietly inflating auto production costs. Here's who pays, who profits, and what it means for the EV transition.

Nations obsessed with military deterrence have discovered a more powerful lever—critical minerals. How the race for rare earths is reshaping geopolitics, supply chains, and global security.

Thoughts

Share your thoughts on this article

Sign in to join the conversation