China's EV Export Boom Is a Survival Story, Not Just Ambition

Chinese automakers are flooding global markets with electric vehicles — but the real driver isn't just geopolitical ambition. It's brutal economics at home. Here's what investors and industry watchers need to know.

Every Chinese EV that rolls off a ship in Rotterdam or Bangkok is partly a statement of ambition — and partly an admission that selling the same car at home barely pays the bills.

The narrative around China's electric vehicle exports tends to focus on geopolitics: Beijing's industrial strategy, the threat to Western automakers, trade war flashpoints. All of that is real. But strip away the grand framing, and a more mundane story emerges — one driven by overcapacity, collapsing margins, and the oldest business logic in the book: go where the money is.

What's Actually Happening Inside China's EV Market

China's domestic EV market is, by any measure, a success. New energy vehicles (NEVs) now account for roughly 40% of all new car sales in the country — a penetration rate that Europe and the United States can only watch with envy. BYD alone sells over 300,000 vehicles a month.

But success at scale has come with a brutal side effect: a price war that is destroying margins across the industry. At peak, China had over 500 registered EV brands. Hundreds remain. The result is a race to the bottom. Tesla has cut prices in China multiple times. BYD's entry-level Seagull sells for under $10,000. The company is essentially daring competitors to match it — and losing money on every unit is a viable strategy only if you're big enough to outlast everyone else.

Government purchase subsidies, which turbocharged adoption for years, were officially wound down at the end of 2022. Some support has returned in modified forms, but nowhere near the levels that once cushioned manufacturers from the market's cold math. For dozens of mid-tier brands, the domestic arena is no longer a growth opportunity — it's a slow bleed.

The Margin Math That Explains Everything

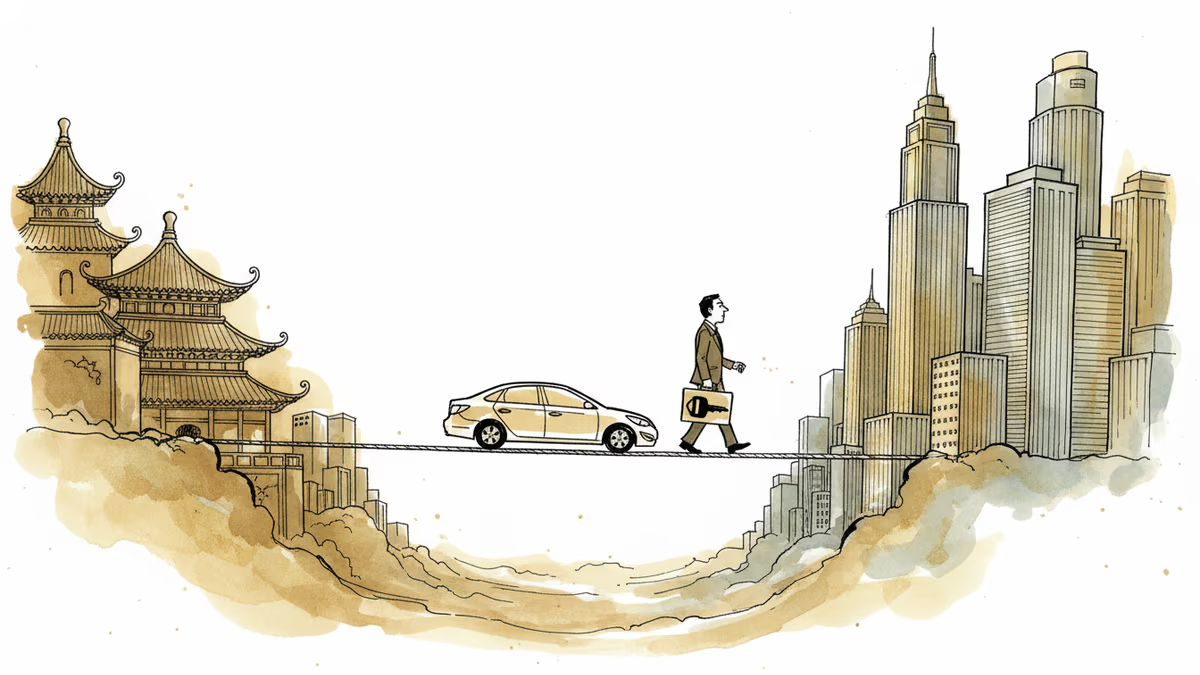

Here's the number that explains the export surge: a Chinese EV sold in Europe fetches 30 to 50% more than the same vehicle sold at home. BYD's Atto 3, for instance, retails at around €40,000 (roughly $43,000) in European markets — nearly double its Chinese sticker price.

For manufacturers squeezed at home, overseas markets aren't just a growth opportunity. They're a financial lifeline. The strategic logic is clean: build volume and brand recognition domestically, extract margin internationally. It's not unlike what Japanese and Korean automakers did in earlier decades — except compressed into a far shorter timeframe and at far greater scale.

The barriers are rising, though. The EU voted in 2024 to impose additional tariffs of up to 35.3% on Chinese EVs, stacked on top of existing duties. The United States has gone further, with tariffs hitting 100% — effectively shutting the door. But Chinese manufacturers are not standing still. They're pivoting to Southeast Asia, the Middle East, Latin America, and Africa: large, fast-growing markets where trade barriers are lower and BYD or SAIC logos are still relatively unfamiliar.

Who Wins, Who Loses — and What It Means for Your Portfolio

The clearest winners, at least in the short term, are consumers in emerging markets. Affordable EVs from China are accelerating adoption in countries where a $25,000 electric car was previously unthinkable. Global EV penetration gets a boost that no Western policy initiative alone could deliver.

The losers are more complicated. Inside China, smaller EV brands are already failing in significant numbers — a shakeout that economists and analysts have long predicted. Local governments that poured subsidies and land into EV manufacturing hubs are now sitting on bad loans and idle factories.

For Western and Korean automakers, the competitive pressure is structural, not cyclical. Hyundai and Kia are contesting the same Southeast Asian markets where BYD is building local factories. Volkswagen, Stellantis, and Renault face a Chinese competitor in Europe that, even with tariffs, can undercut on price. Hyundai's stock fell roughly 20% in 2024, with China-driven pricing pressure cited as a contributing factor alongside broader EV demand softness.

For investors, the question isn't simply whether to buy or avoid Chinese EV stocks. It's about understanding second-order effects: battery suppliers, charging infrastructure players, and legacy automakers all carry exposure to this competitive dynamic. CATL, which supplies batteries to both Chinese and Western brands, sits at an interesting intersection — benefiting from volume growth while navigating geopolitical scrutiny.

The Limits of the Export Strategy

It would be a mistake to read Chinese EV exports as a guaranteed march to global dominance. The challenges are real. Building brand trust takes time and money. After-sales service networks in unfamiliar markets are expensive to establish. BYD has quietly revised its European sales targets downward more than once.

There's also the question of what happens if major export markets close their doors further. A coordinated tariff response from the EU, UK, and key Southeast Asian economies — however unlikely — would force a reckoning with the domestic overcapacity that exports are currently masking.

And beneath the export surge lies a structural question that no one has fully answered: can China's EV industry consolidate fast enough to become sustainably profitable, or will state support keep too many marginal players alive for too long?

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Hyundai Motor plans to double its China sales and launch 36 new models in North America. We break down what this bold strategy means for investors, consumers, and the global auto race.

Containers are piling up at the wrong ports while freight rates surge. Here's what's driving the imbalance, who's winning, who's losing, and what it means for inflation and global trade.

Trump is building a coalition to reopen a critical global waterway. The stakes go beyond shipping lanes — they touch inflation, energy prices, and the limits of American leverage.

Iran's Hormuz Strait blockade disrupts Japan's massive used car exports, creating ripple effects across global automotive markets and consumer prices.

Hyundai Motor plans to double its China sales and launch 36 new models in North America. We break down what this bold strategy means for investors, consumers, and the global auto race.

Containers are piling up at the wrong ports while freight rates surge. Here's what's driving the imbalance, who's winning, who's losing, and what it means for inflation and global trade.

Trump is building a coalition to reopen a critical global waterway. The stakes go beyond shipping lanes — they touch inflation, energy prices, and the limits of American leverage.

Iran's Hormuz Strait blockade disrupts Japan's massive used car exports, creating ripple effects across global automotive markets and consumer prices.

Thoughts

Share your thoughts on this article

Sign in to join the conversation