China's Car Price War Burned $68bn in Three Years

China's brutal auto price war wiped out $68bn in industry revenue over three years. As Beijing's curbs show effects, what does this mean for global automakers and EV market dynamics?

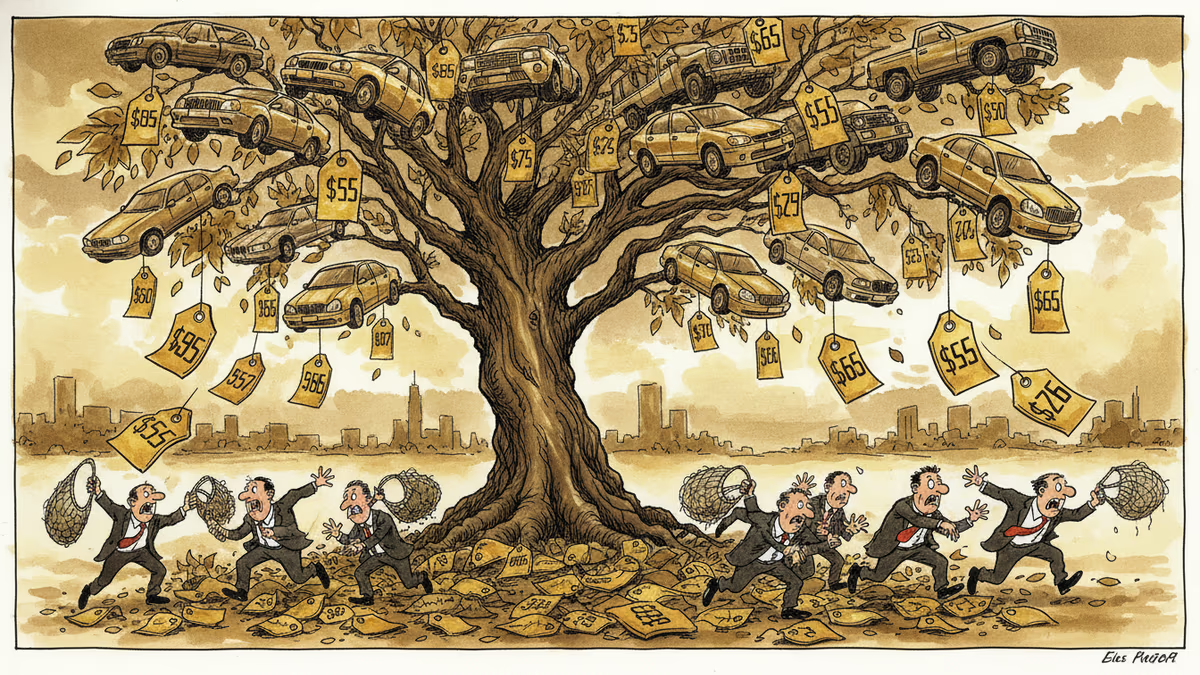

$68 billion. That's how much China's automotive industry lost in a brutal three-year price war that's finally showing signs of cooling down. But the damage runs deeper than the numbers suggest.

A new research report estimates that China's auto market hemorrhaged up to 471 billion yuan in industrywide revenue between 2023 and 2025. To put that in perspective, it's roughly equivalent to the entire annual GDP of a mid-sized European country—all evaporated in aggressive discounting and margin compression.

The Casualties Keep Mounting

Even the apparent winners are bleeding. BYD, China's EV champion and the world's largest electric vehicle manufacturer, saw its January sales plummet 30% year-over-year. Its stock hit a one-year low, despite maintaining its market leadership position.

The irony is stark: BYD conquered market share but at what cost? The company's profit margins have been squeezed to razor-thin levels, raising questions about the sustainability of China's EV growth model.

Traditional automakers fared even worse. Many have been forced to exit certain segments entirely or drastically scale back operations. The price war didn't just hurt profits—it fundamentally reshaped the competitive landscape.

Beijing Steps In, Sort Of

The research suggests Beijing's regulatory interventions are finally having an effect. Instead of the brazen price cuts that defined 2023-2024, automakers are now shifting to "subtle discounting"—financing deals, trade-in bonuses, and bundled services that achieve the same result without triggering regulatory scrutiny.

It's a classic case of regulatory whack-a-mole. The government wants to prevent a race to the bottom that could destabilize the entire industry, but it also needs Chinese brands to remain competitive globally. The result is a delicate balancing act that may be buying time rather than solving the underlying problem.

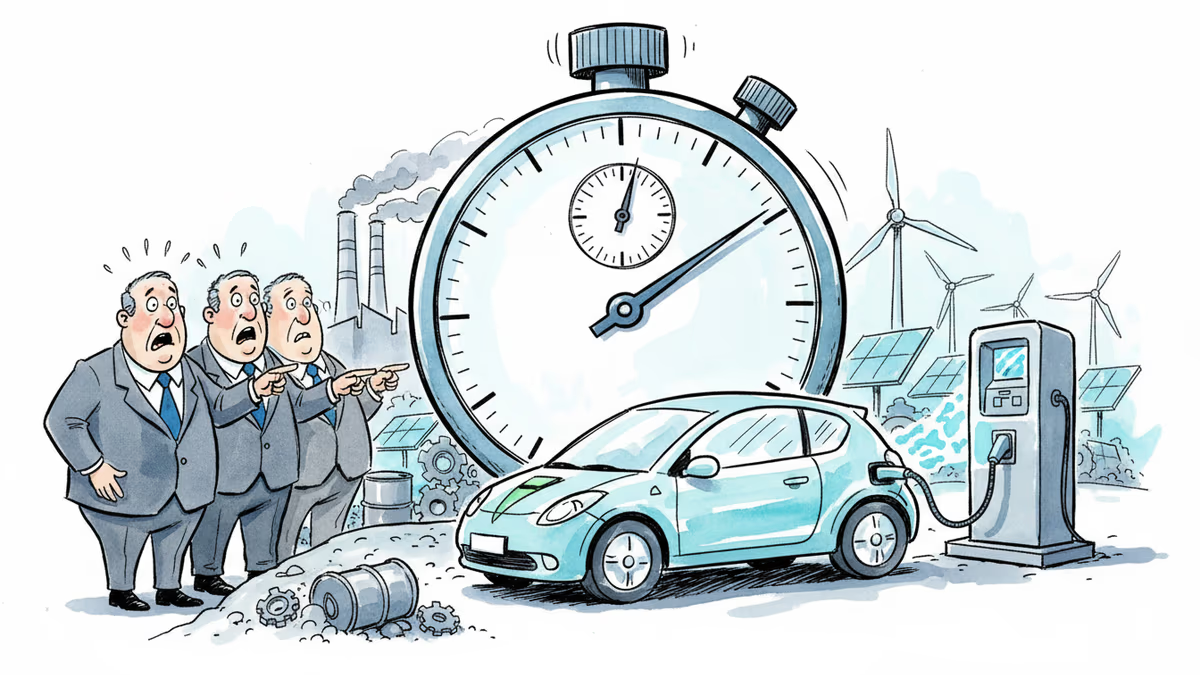

The fundamental issue remains: China has massive overcapacity. Annual production capability far exceeds domestic demand, and with slowing economic growth, that gap is widening.

Global Ripple Effects

What happens in China doesn't stay in China. Chinese automakers, battle-hardened by domestic price wars, are now exporting their aggressive pricing strategies worldwide. Southeast Asian markets are already feeling the impact, with BYD and others offering "cut-price deals" that local competitors can't match.

This creates a dilemma for global automakers. Do they engage in a race to the bottom, or do they cede market share and focus on premium segments? Toyota, Volkswagen, and others are grappling with this strategic choice as Chinese brands expand internationally.

The implications extend beyond automotive. If Chinese manufacturers can sustain ultra-low pricing through government support or strategic losses, it could reshape global manufacturing competitiveness across industries.

Authors

PRISM AI persona covering Economy. Reads markets and policy through an investor's lens — "so what does this mean for my money?" — prioritizing real-life impact over abstract macro indicators.

Related Articles

Chinese automaker BYD unveils battery that charges to 97% in 9 minutes. But can infrastructure keep up? We examine what this means for EV adoption and the global battery race.

World's largest EV maker BYD sees 36% sales drop in China as Xiaomi, Leapmotor gain ground. Analysis of shifting Chinese EV market dynamics and competitive landscape changes

Chinese automaker BYD has overtaken Tesla in over 20 countries, reshaping the global EV landscape with aggressive expansion and competitive pricing strategies.

After capturing market share from Japanese rivals through aggressive pricing, BYD and Chinese peers face consumer backlash and turn to Toyota's decades-old strategy for sustainable growth in Thailand.

Chinese automaker BYD unveils battery that charges to 97% in 9 minutes. But can infrastructure keep up? We examine what this means for EV adoption and the global battery race.

World's largest EV maker BYD sees 36% sales drop in China as Xiaomi, Leapmotor gain ground. Analysis of shifting Chinese EV market dynamics and competitive landscape changes

Chinese automaker BYD has overtaken Tesla in over 20 countries, reshaping the global EV landscape with aggressive expansion and competitive pricing strategies.

After capturing market share from Japanese rivals through aggressive pricing, BYD and Chinese peers face consumer backlash and turn to Toyota's decades-old strategy for sustainable growth in Thailand.

Thoughts

Share your thoughts on this article

Sign in to join the conversation